What is an ICHRA Health Plan?

Offering healthcare benefits to your workforce isn't as simple as it sounds.

You need to think about your budget, what your employees need, and your level of risk tolerance.

Traditional health insurance plans tend to learn too much in one direction — giving you more cost control at the expense of flexibility and vice versa. Then, there are plans like ICHRA, which strike a balance between these considerations.

Here's a closer look at ICHRA, how it works, why it's important, and how to make the most out of it.

What is ICHRA (Individual Coverage Health Reimbursement Arrangement)?

ICHRA — short for "Individual Coverage Health Reimbursement Arrangement" — is a type of health insurance plan for businesses where customizability and cost control converge.

How Does ICHRA Work?

Implementing an ICHRA plan starts with the employer, but also involves the participation of employees down the pipeline.

Here is a breakdown of the steps in a typical ICHRA setup:

- Setting a budget — The first order of business is to set a maximum reimbursement allowance that you'll cover for qualifying medical expenses. It's common for businesses to set different allowances for various employee groups, such as full-time employees, part-time employees, and interns.

- Bear in mind that eligible doesn't equate to mandatory in the context of ICHRA plans.

- Notification and enrollment — Employees are then informed if they're qualified for the ICHRA plan. They're also briefed on how it works, the benefits, and the deadline for enrollment.

- Reimbursing expenses — Once enrolled, employees can shop for individual health insurance plans and other eligible services. Upon submission of proof, the employer reimburses the amount up to the maximum allowance per person.

- Ongoing management — While employees are responsible for buying their own healthcare, employers or third-party providers are in charge of administrative tasks. This includes compliance with regulatory requirements, maintaining records, and making fine adjustments to improve the plan's efficiency over time.

To get an idea of how ICHRA works in practice, suppose the company provides a maximum allowance of $500 per person.

An eligible employee then purchases a health insurance product with premiums costing $550 per month. Under the ICHRA plan, the company only reimburses $500 while the employee shoulders the excess out of pocket.

Pros of ICHRA

- Cost control — Being able to set a maximum allowance per person makes ICHRA ideal for employers that prioritize predictability and risk management.

- Customizability — Rather than rigid plans, employees will be able to tailor their healthcare to their specific needs.

- Tax benefits — ICHRA reimbursements are considered business expenses, while monthly payments are also non-taxable.

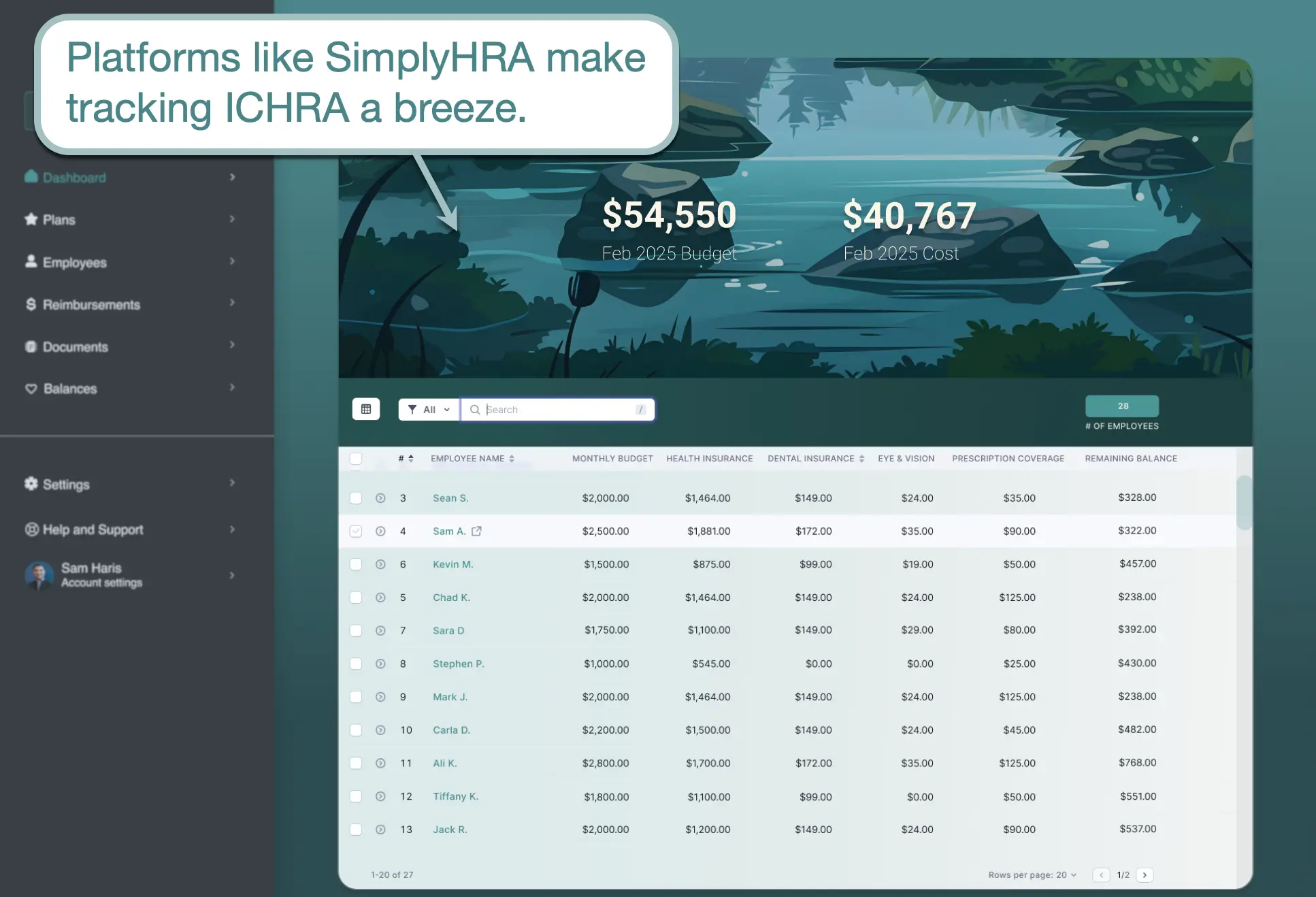

- Streamlined management — Platforms like SimplyHRA streamline ICHRA management while also offloading time-consuming tasks like compliance.

- Portability — Since employees purchase individual health insurance plans, they get to keep those benefits even after they leave your company (you simply stop reimbursing them for premiums).

Potential Drawbacks of ICHRA

- Learning curve — Both employer and employee will need an adequate understanding of the fine details of ICHRA plans to be effective.

- Requires employee research — Apart from understanding how ICHRA works, employees may need help comparing plan costs and understanding how affordability affects premium tax credit eligibility. For 2026, the affordability percentage is 9.96%; employees offered an affordable ICHRA generally cannot receive a Marketplace premium tax credit, while those offered an unaffordable ICHRA may opt out and may qualify if otherwise eligible.

- Dependent on individual markets — The coverage, costs, and availability of plans heavily rely on the individual health insurance market, which can lead to inconsistent benefits per person and potential uncertainty in the future.

Best Practices for Implementing ICHRA for Your Business

To help your business stay profitable and healthy with ICHRA, here are five best practices you should remember:

- Provide accessible learning resources — Share guides, fact sheets, and other resources (like SimplyHRA's 24/7 chatbot) to help employees and admins learn all about ICHRA.

- Set realistic reimbursement amounts — Be sure to align your monthly ICHRA allowances with your workforce's specific healthcare needs (for example, workers performing physically demanding tasks may have different needs than employees in an office setting).

- Prioritize transparency and open communication — Give employees a channel for voicing their feedback on your ICHRA plan.

- Review and improve your plan over time — Review monthly budgets, reimbursements, and benefits over time to optimize and improve your plan over time.

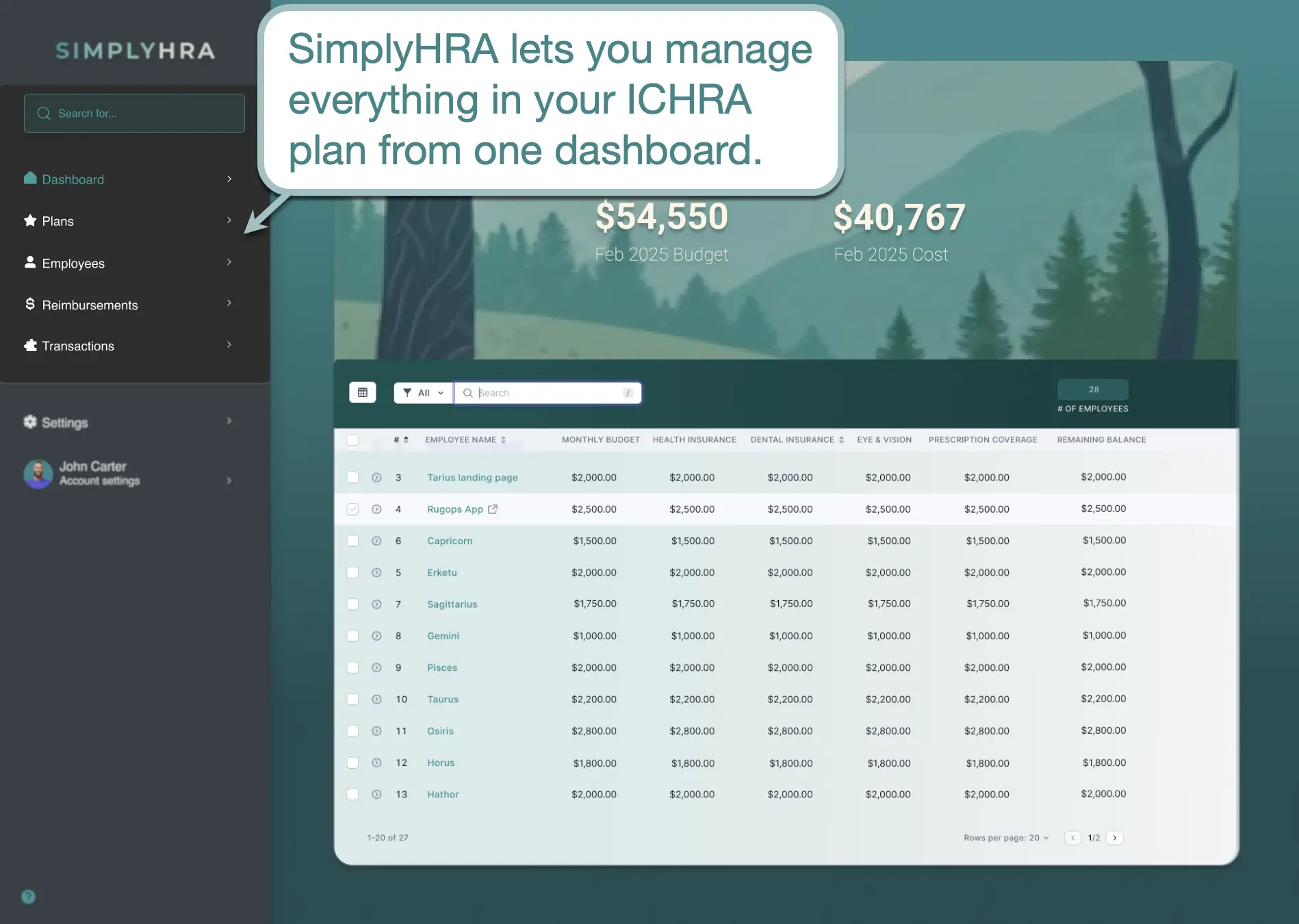

- Invest in the right ICHRA platform — Streamline everything through a centralized ICHRA management platform like SimplyHRA to track budgets, manage reimbursements, and simplify reporting.

Managing Your ICHRA Plan with SimplyHRA

Considering a switch to ICHRA for employee health benefits?

SimplyHRA is an all-in-one platform that can help you through the entire process — from setting reimbursement allowances to compliance.

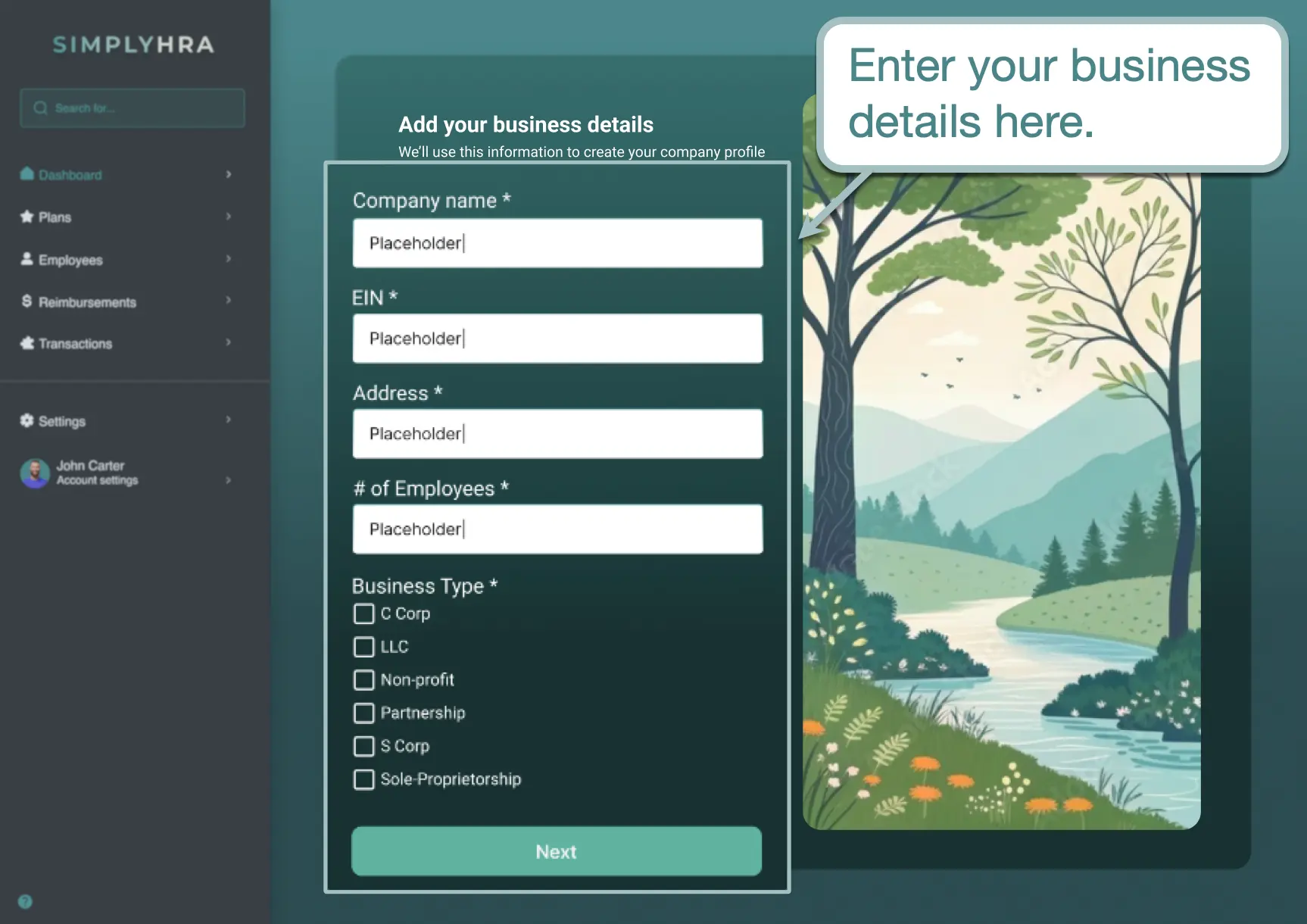

After creating an account, the next step is to enter your business details, including your company name, EIN, and business type.

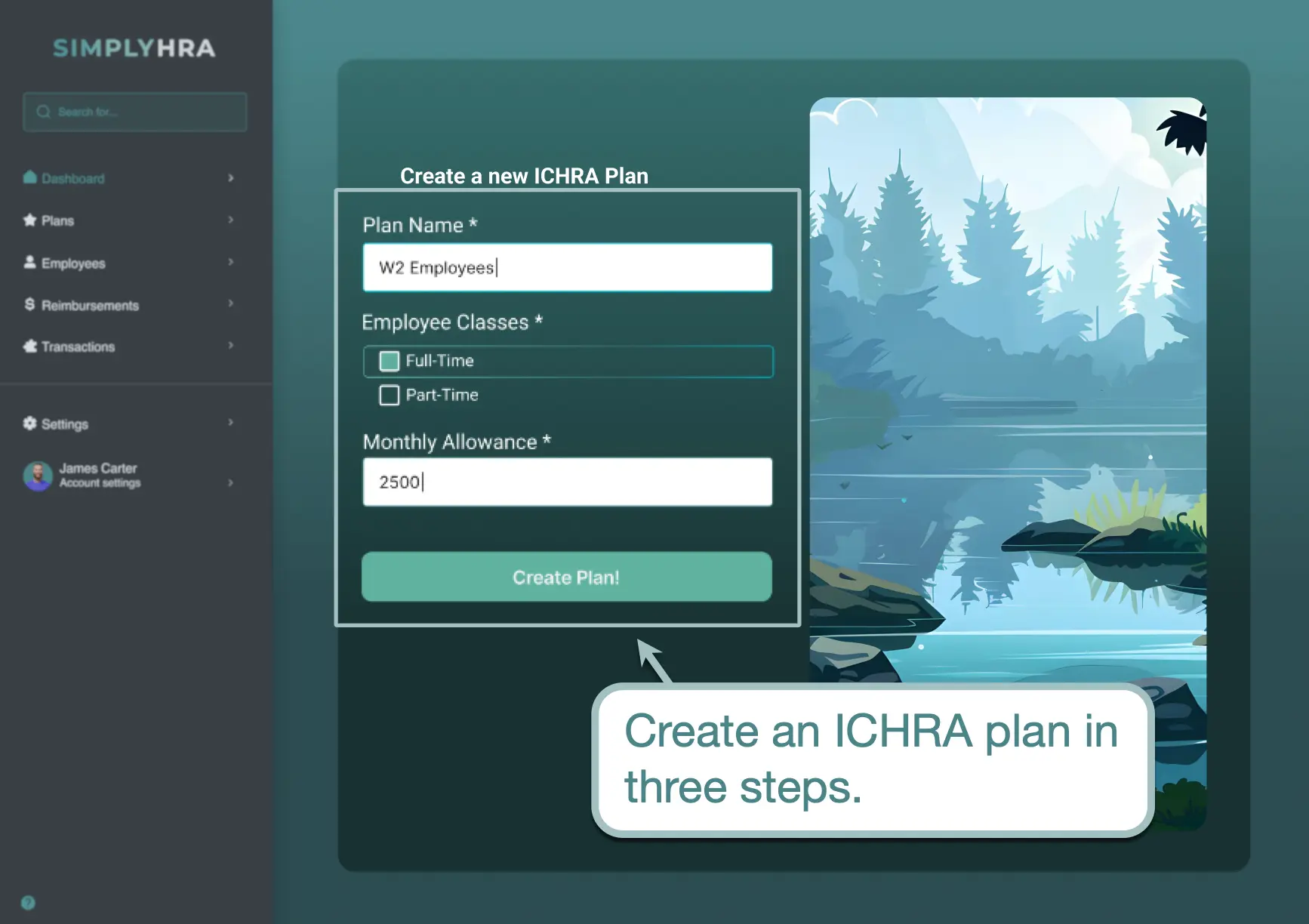

The initial setup will guide you through the creation of your first ICHRA plan. This is as easy as setting a plan name, specifying the employee class, and entering the monthly allowance per person.

Once your plan is created, you're immediately redirected to your dashboard where you can onboard employees, track your budget, and monitor transactions — all in one place.

Frequently Asked Questions

Before we wrap up this post, let's go over a few FAQs surrounding ICHRA to help you create an optimal healthcare plan for employees:

What's the Difference Between ICHRA and QSEHRA?

There are a few differences between ICHRA and Qualified Small Employer Health Reimbursement Arrangement (QSEHRA).

For one, ICHRA can be used by businesses of all sizes, whereas QSEHRA can only be offered by companies with fewer than 50 employees. ICHRA also offers more flexibility and autonomy to employees in terms of benefits.

Are ICHRA payouts taxed?

No, reimbursements through an ICHRA plan are not taxable.

In fact, employer contributions to ICHRA are accounted for as business expenses. At the same time, the amount received by employees is also not considered taxable income.

What are other alternatives to ICHRA?

Apart from ICHRA, there are other types of Health Reimbursement Arrangements (HRAs) available to businesses. This includes QSEHRA, Group Coverage HRA (GCHRA), and Excepted Benefit HRA (EBHRA).

Getting Started with SimplyHRA

Overall, ICHRA provides employers with a cost-effective and low-risk option to provide flexible healthcare benefits to their employees.

Just remember that employees will be responsible for the legwork in terms of researching and purchasing healthcare products. They'll need all the support they can get to make the right, sustainable decision.

With SimplyHRA, you can simplify the technical aspects of ICHRA, leaving you free to focus on providing the education they need. See it in action by requesting a free demo here!

Related blogs

Does My Health Plan Qualify for an ICHRA? A Plan-by-Plan Guide

SimplyHRA vs Take Command