How Does Group Insurance Differ from Individual Insurance? 6 Questions Answered

Group insurance versus individual health insurance:

How are they different?

Although both insurance plans offer the necessary health benefits, your chosen insurance has a profound impact on your balance sheet and — of course — your employees' access to healthcare.

Before you make a decision, you need to understand the key differences between the two.

Group Insurance vs. Individual Insurance: What are the Differences?

Both group and individual insurance plans can provide the essential health benefits your employees need, such as medical coverage and preventative care. But there are crucial differences between them in terms of factors like costs, coverage options, and eligibility.

1. What is Group Health Insurance?

From the name itself, group insurance provides coverage and benefits to a group of people.

Employers get to select a group insurance plan (or set of plans) based on their needs, size, and budget. As for employees, each member is covered by their own policy with benefits they can enjoy individually.

Group insurance has a handful of benefits for both employers and employees.

For one, the cost of the premium is spread between the company and its employees, increasing affordability. And since group insurance is essentially a bulk offer, the actual per-person cost of coverage can be lower than with individual insurance.

2. How do Group Insurance Plans work?

Around 165 million Americans are protected by employer-sponsored or shared-cost insurance plans.

Here's how it works:

- Deciding eligibility — The company chooses who among the workforce is eligible for the group insurance plan. Full-time employees then have the option to enroll or decline coverage.

- Selecting the group insurance plan — The company selects which group insurance product to buy.

- Sharing the cost — Since group insurance costs and risks are shared between the company and employees, the per-person cost is much lower than individual health insurance plans. Employers generally cover a bigger portion of the premiums than employees.

3. What is Individual Health Insurance?

Individual health insurance is a plan that employees purchase on their own — without any assistance from their employer or a federal government program.

This type of insurance can be bought from a private or a public health exchange, like the federal or state Health Insurance Marketplace. Employees can also buy directly from health insurance companies, with or without an agent or broker.

Individual health insurance plans are perfect for the self-employed, unemployed, or full-time employees working for small companies (fewer than 50 employees) that are not obligated to purchase group insurance. Don't forget that individual health insurance is also more portable than group insurance plans, which are tied to the employer.

4. How Does It Work?

Unlike group insurance where the company manages almost everything, obtaining individual health insurance is the mainly the employees' responsibility.

- Selecting the plan and coverage — Employees are free to choose the policy and coverage of their individual insurance plans. This gives them more control in terms of benefits, deductibles, out-of-pocket maximums, and so on.

- Paying for premiums — Employees are solely responsible for paying their insurance premiums. While this can be more expensive, individual insurance provides an opportunity for policyholders to tailor their plans to their personal or family needs.

- Choosing a provider — Employees can choose between private and public health exchanges. Many individuals prefer to purchase their insurance plans through state or federal marketplaces to take advantage of programs like the Affordable Care Act (ACA).

As an employer, you can offer employees the benefits of individual health insurance without the unpredictability through an Individual Coverage Health Reimbursement Arrangement (ICHRA). With ICHRA, employees have the autonomy to choose and purchase their own health insurance plan while employers reimburse a portion of the costs up to a maximum allowance.

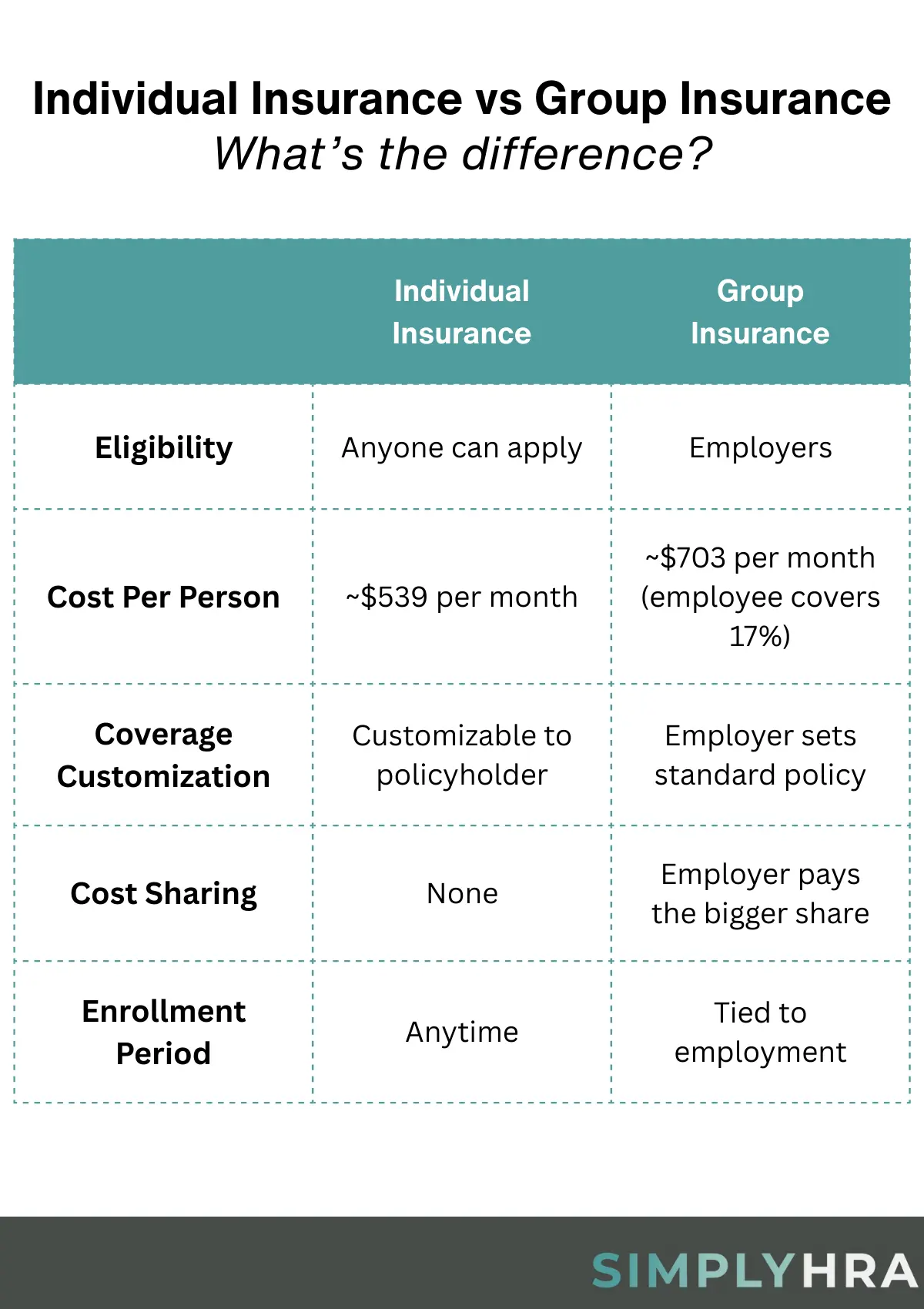

5. What Are The Key Differences Between Group Insurance And Individual Insurance?

According to a 2026 study by the Kaiser Family Foundation (KFF), group insurance costs about $703 per month or about $8,435 annually for employee-only coverage. Family coverage, on the other hand, costs about $1,997 per month or $23,964 a year.

Take note that, in these plans, employees shoulder 17% to 28% of the premiums.

On the other hand, individual health insurance premiums cost an average of $539 a month or $6,468 a year for self-only coverage plans.

Just remember that this amount varies per state. For example, in Wyoming, the average cost of individual health insurance sits at $791 per month.

Apart from the costs, individual and group health insurance also differ in terms of coverage options, eligibility, customization, and plan management.

Individual health insurance frees companies from the responsibilities of purchasing and maintaining coverage for their workforce. It also gives employees more control and legroom for benefits beyond what companies offer in standard group insurance policies.

6. Which Is Better For Small Businesses?

In terms of choosing between group and individual health insurance, both have their own pros and cons.

Group health insurance makes perfect sense for small businesses from a cost standpoint. Not only will your per-person payments be lower, offering group coverage is also simpler to manage and more attractive to employees — not to mention that group insurance premiums also lead to huge tax savings.

However, the price of group health insurance plans may increase due to market concentration and unpredictable utilization. Some employees may also look for plans that better fit their coverage needs, like specialist therapies, critical illnesses, dental, and maternal care.

These employees have no choice but to decline the company's standard group coverage and seek their own insurance plan.

This is where ICHRA steps in.

ICHRA lets both employees and employers get the best of both worlds. Not only does it pool the risk and share the costs, it also allows employees with specific needs to access the healthcare services and coverage they require.

The good news is, offering ICHRA is easier than ever.

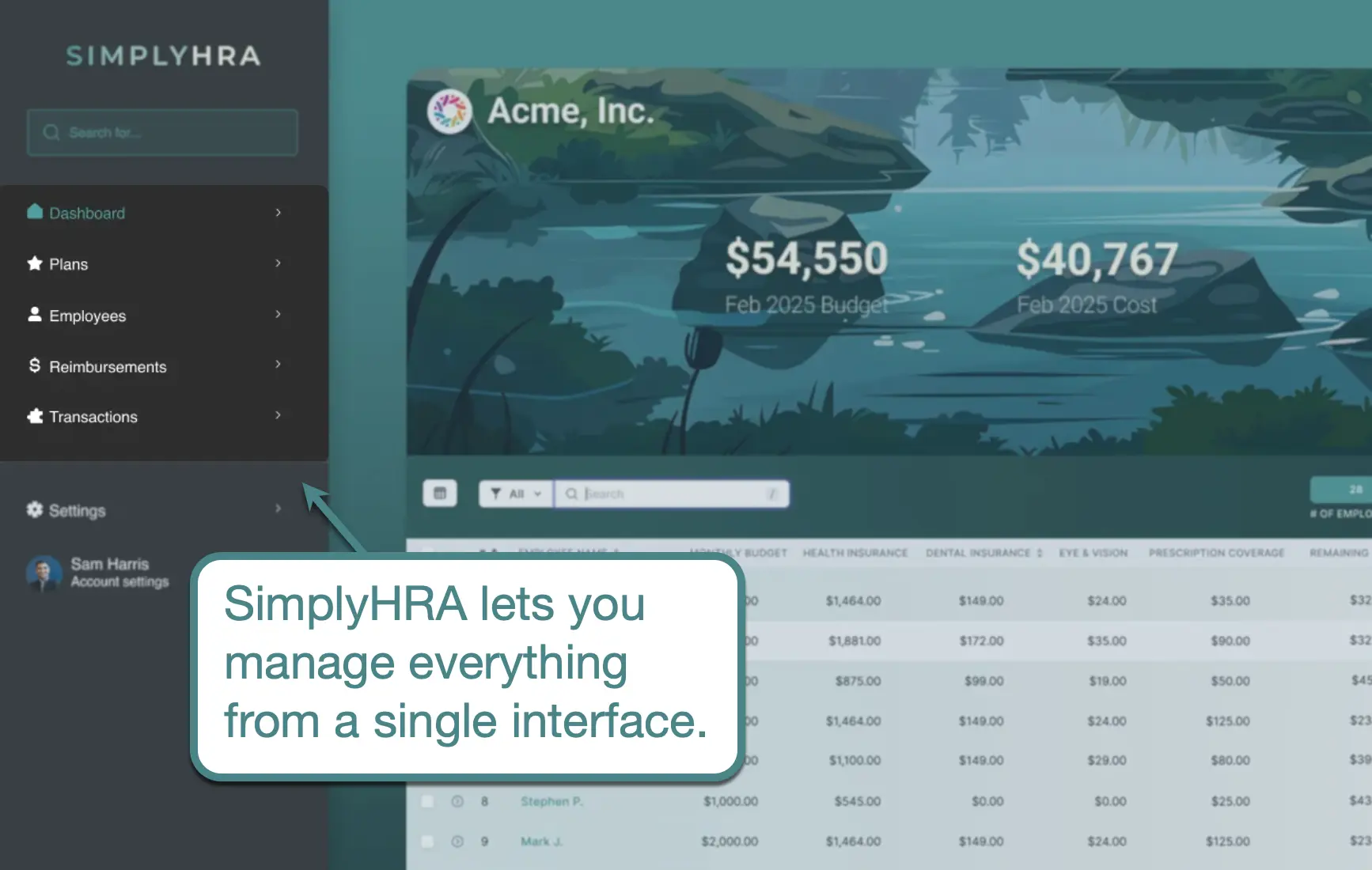

SimplyHRA is a health benefits management platform for businesses.

Using the visual interface, you can set your own budget per employee group, set your reimbursement amounts, onboard your employees, and more — the software will handle everything else from expense management to compliance.

Conclusion

Both individual and group health insurance plans can offer essential health benefits that most high-value employees need.

While individual health insurance is more customizable, group insurance is more cost-effective per covered person.

ICHRA fits in the middle ground between the two insurance types — keeping companies in control of the costs while offering flexibility for employees with specific needs.

SimplyHRA is the perfect gateway for businesses to get started with ICHRA. Book a demo here to see it in action.

Related blogs

Replace Group Health in 2026: ICHRA Guide for Employers

Individual vs Group Health Insurance 2026: Which Is Better?