Best Health Insurance for Small Business Owners: The Top Options Compared 2026

Adopting a health insurance plan is not an overnight decision for small businesses.

You need to look into factors like costs, benefits, and your firmographics to ensure you pick the right option for your employees.

One of the first steps, of course, is to understand the different types of health insurance available, like:

- Individual Coverage Health Reimbursement Arrangement (ICHRA)

- Qualified Small Employer Health Reimbursement Arrangement (QSEHRA)

- Fully-Insured Group Health Plans

- Self-Funded Health Plans

- Level-Funded Health Plans

- Association Health Plans (AHPs)

In this post, we'll do a thorough breakdown of these insurance types, their benefits, and some potential drawbacks. To accelerate your search, we'll also look at the top health insurance providers and platforms in the market.

But first, let's go over why health insurance is important for small businesses in the first place.

Importance of Health Insurance for Small Business Owners

First and foremost, providing health insurance is a legal obligation if you have 50 or more employees. But that's not the only reason why you should invest in coverage for your employees:

1. Attract and Retain Talent

Offering health insurance for your employees will make your company more resilient to labor shortages, even in tight markets.

Keep in mind that every worker wants and deserves coverage — be it for them as an individual or for their entire family. With a solid health insurance plan, you boost your company's ability to attract and retain employees.

2. Get Tax Benefits

Providing health insurance unlocks different tax benefits that will put your small businesses in a more favorable financial position.

For one, qualifying group health insurance plans are 100% tax deductible. Paying premiums can also reduce payroll taxes and make you eligible for tax credits — leading to thousands of dollars in potential savings.

3. Increase Productivity and Morale

It's no secret that employees prefer to be in companies where they feel valued.

Offering health benefits tailored to their needs is a great way to convey this message. And with the peace of mind afforded by coverage, your employees can remain laser-focused on productivity.

4. Maintain a Healthy Workforce

Finally, you can't ignore the main reason why health insurance plans are designed in the first place.

The goal is to provide workers access to the healthcare services they need, which may include cholesterol screening, routine vaccinations, and even mental health services. By establishing a health conscious culture, you're looking at fewer sick days and an overall more productive team.

Challenges Faced by Small Business Owners

Despite the obvious advantage of providing health insurance, some companies struggle with a few challenges when choosing the right coverage provider.

This includes:

- Limited budget

- Increasing health insurance costs

- Lack of understanding on key processes (i.e., enrollment)

The good news is, any employer can address these challenges just by understanding the types of health insurance plans they can purchase.

Individual Coverage Health Reimbursement Arrangement (ICHRA)

ICHRA is slowly but steadily gaining ground in the health benefits market, and for plenty of good reasons.

This type of health insurance enables companies to control how much they spend on employee benefits. At the same time, it provides employees the autonomy to choose which plan to purchase based on their needs.

It is the perfect middle ground between group insurance and individual insurance plans — providing predictability, cost-efficiency, and flexibility all at once.

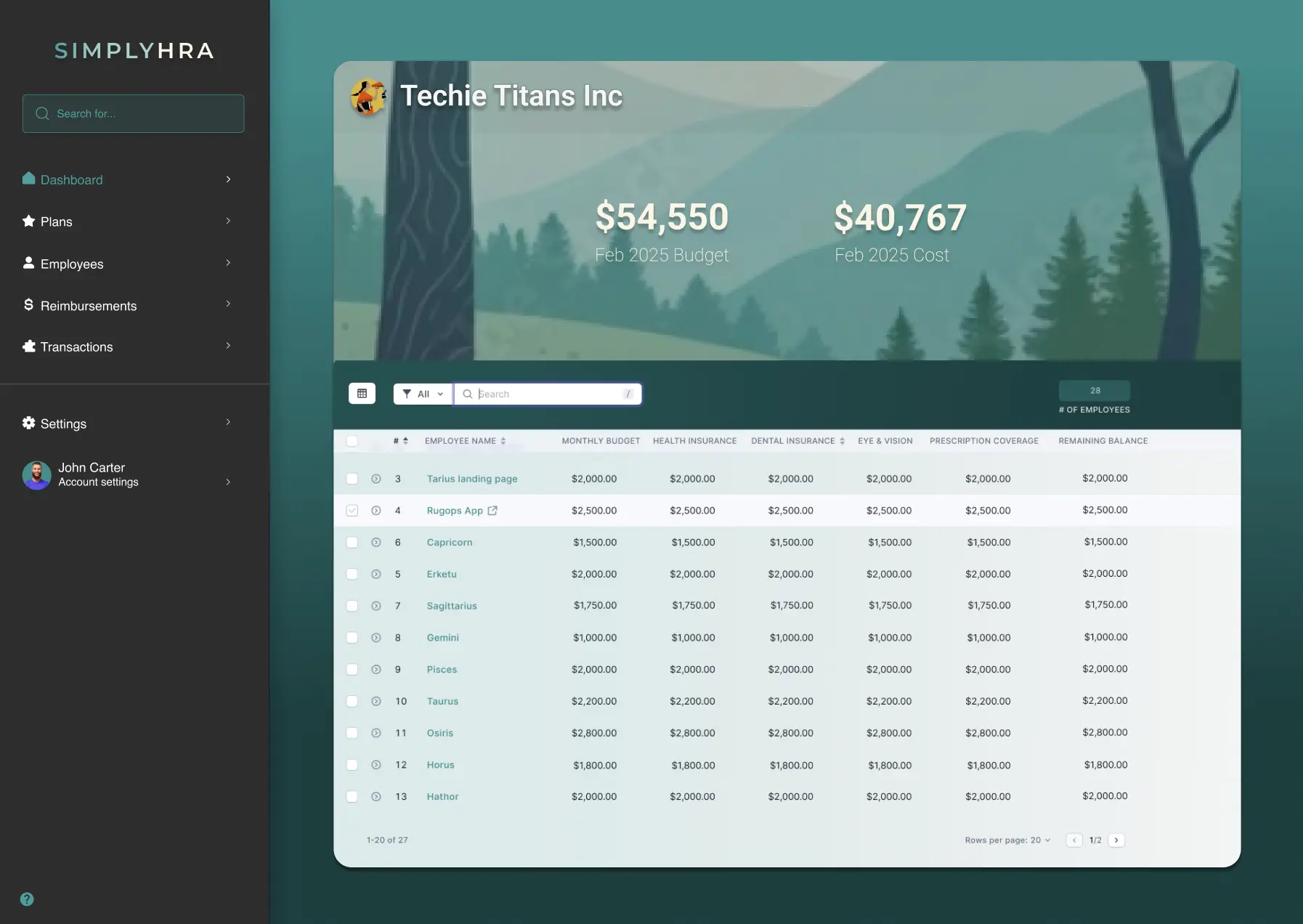

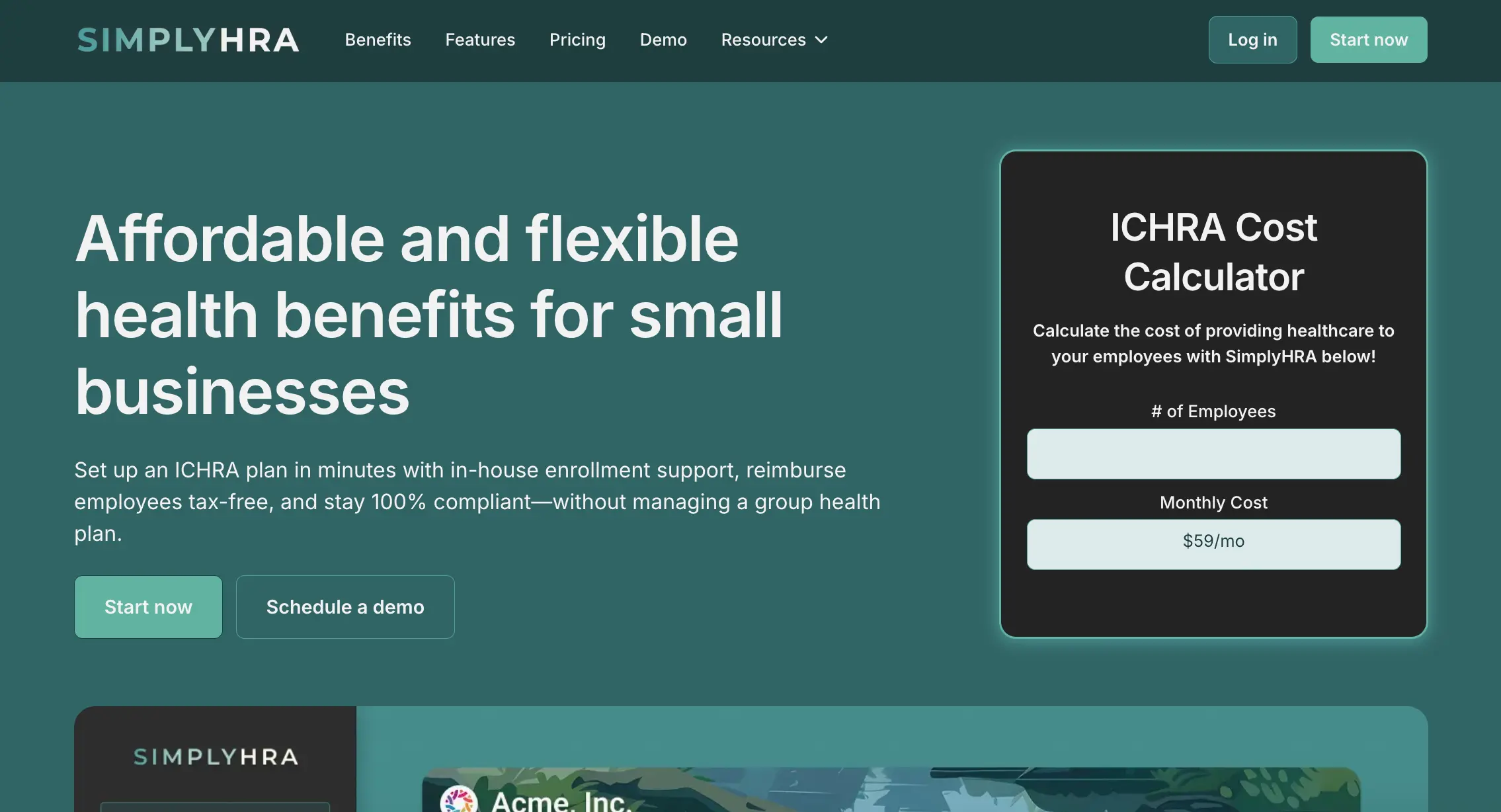

SimplyHRA is one of the premier platforms offering ICHRA solutions to businesses of any size. It provides a centralized dashboard where you can manage your budget, track payouts, customize reimbursement plans, and more.

Related Resource: Check out our 2026 ICHRA Affordability Guide to ensure your reimbursement plans meet the latest 9.96% compliance threshold.

The main disadvantage of ICHRA is that it offloads the responsibility of choosing a health insurance plan to your employees. This stressful experience can lead to rushed decisions and unintended coverage gaps.

That's why it's important for businesses to approach ICHRA with employee education in mind. It's also important to invest in a platform like SimplyHRA to streamline the budget tracking and reimbursement request processes for your entire team.

To see it in action, click here to request a personalized demo.

Qualified Small Employer Health Reimbursement Arrangement (QSEHRA)

Similar to ICHRA, QSEHRA also enables employees to pick their own insurance with the help of reimbursements allocated by their employer.

The key difference is, QSEHRA is only available to eligible employers that are not Applicable Large Employers and that do not offer a group health plan to any employees. And while ICHRA lets employers tailor different allowance amounts to multiple employee classes, QSEHRA only permits variation by age and family size within the applicable rules.

While QSEHRA plans are more budget-friendly than ICHRA, take note that it comes at the expense of lower customizability and annual contribution limitations set by the Internal Revenue Service (IRS).

Fully-Insured Group Health Plans

Of course, there's the traditional employer-sponsored group health plan — covering thousands of employees in the U.S. under small to mid-sized companies.

The premise of fully-insured plans is simple: a blanket insurance policy that all employees can either decline or enroll in.

This straightforward approach offers simplicity and predictability. The insurer also takes on the risk of claims, which can be appealing for businesses still fighting for stability.

In terms of downsides, fully-insured group health plans rely solely on a pre-designed policy.

Once the employer chooses one of the options, there's little to no flexibility in terms of coverage and costs. Premiums are also highly affected by macroeconomic trends, like economic growth, inflation, and employment rate.

Self-Funded Health Plans

In a self-funded health plan, a company primarily pays for qualifying medical claims out of pocket — without the need for a third-party insurer. This gives companies total control over health benefits, costs, and employee eligibility.

Self-funded health plans are also highly scalable, which contributes to their popularity in the U.S.

According to KFF, 67% of covered workers were enrolled in self-funded health plans in 2025, a share similar to recent years.

The downside is that companies themselves absorb the majority of the financial risk of paying for claims. This requires a degree of liquidity and optimal cash flow management.

Level-Funded Health Plans

A level-funded health plan borrows elements from fully-insured and self-funded health plans.

With this plan, you pay an external insurer for a stop-loss policy, which kicks in whenever a claim exceeds your allowed healthcare budget per person.

This protects your business from the risk of high, unexpected costs associated with self-funded health plans. And similar to a fully-insured plan, you're sharing the responsibility for claims with a carrier through fixed monthly premiums.

Association Health Plans (AHPs)

Lastly, an AHP is a type of health insurance plan where a group of small businesses or self-employed professionals pool their funds together to pay for coverage as a unified entity.

This brings benefits such as lower premiums, streamlined administrative tasks, and access to coverage options that would otherwise be out of reach.

While the structure of an AHP brings down financial risks, it can lead to other issues like coverage gaps and the possibility of fund mismanagement.

Today, companies and individuals can seek AHP opportunities through Chambers of Commerce and trade associations — both local and national.

Health Insurance for Small Businesses: Top Providers in 2026

Found the type of health insurance that matches your company's needs?

The next step is choosing the right provider or platform to make it happen.

Without further ado, here are the top eight health insurance providers for small businesses:

1. SimplyHRA.com

SimplyHRA is a health benefits platform designed explicitly for managing ICHRA plans.

It provides employers with an intuitive, visual dashboard for creating reimbursement plans, controlling budgets, handling enrollments, and managing payments. SimplyHRA also takes care of the technical aspects of ICHRA on your behalf, including approvals and regulatory compliance.

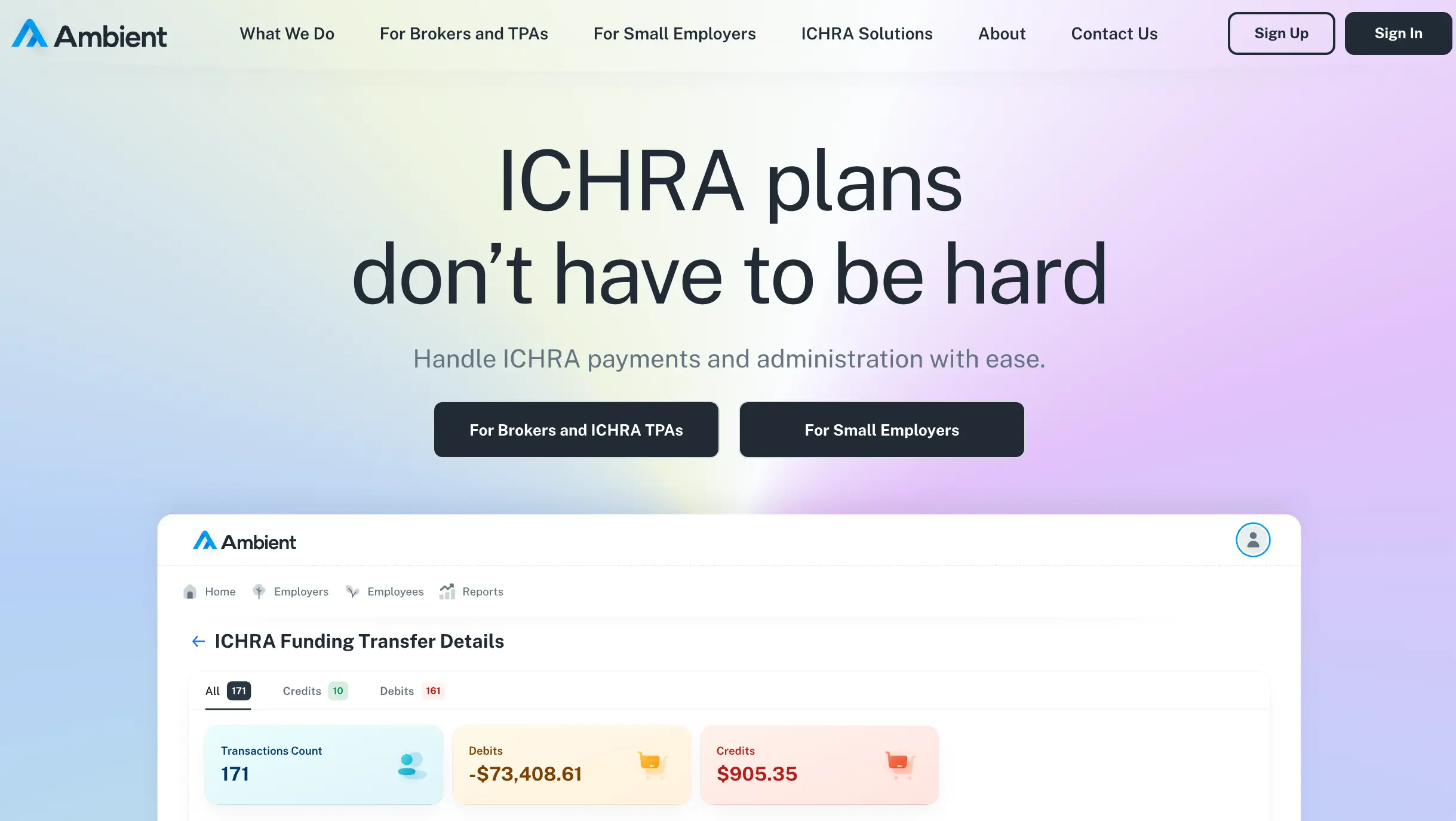

2. Ambient

Ambient is another ICHRA platform built for both small businesses and insurance brokers. It features tools for simplifying administrative tasks as well as automating premium payments and reimbursements.

3. PeopleKeep

PeopleKeep is a flexible health benefits management tool that can be used for offering health reimbursement arrangements, like ICHRA, QSEHRA, and Group Coverage HRA (GCHRA). In addition to a visual management dashboard, the company also offers a wealth of learning resources for new businesses stepping into the health benefits space for the first time — from downloadable guides to a checklist of eligible expenses.

4. Salusion

Salusion also helps businesses create and enforce HRAs, including ICHRA, QSEHRA, and Excepted Benefits HRA (EBHRA). It's created as a one-stop solution for managing every single aspect of HRAs — from compliance to payments.

5. Blue Cross Blue Shield

Blue Cross Blue Shield is a large network of national health insurance companies, covering over 115 million clients and partnering up with millions of healthcare providers. Rather than specializing in a specific type of health insurance, the platform generates a list of insurance plans that match your needs, including level-funded plans, fully-insured plans, and Health Maintenance Organizations (HMOs).

6. Kaiser Permanente

Kaiser Permanente is another comprehensive healthcare plan provider that offers a good range of products for small businesses. In addition to traditional group and individual insurance structures, the company lets you tailor your plan with additional benefits like acupuncture, chiropractic, and vision care.

7. UnitedHealthcare

Finally, UnitedHealthcare is a reputable, national healthcare company offering insurance plans for individuals and employers alike.

It offers a robust set of plans that connect to a massive collective of hospitals and healthcare service providers. And as a large provider of insurance, UnitedHealthcare has the tools, resources, and experienced agents to help you find the perfect plan your employees deserve.

Conclusion

Always remember that every employee deserves health benefits that practically and effectively match their needs.

This is a journey that starts with choosing the right insurance type and provider. Hopefully, the guide above equipped you with all the information you need to make a solid decision.

If you're looking for the perfect compromise between flexibility and cost-effectiveness, your top options would be an HRA — particularly ICHRA or QSEHRA.

Get started today by creating a SimplyHRA account here.

Related blogs

Does My Health Plan Qualify for an ICHRA? A Plan-by-Plan Guide

SimplyHRA vs Take Command