For Employers: Health Benefits That Fit Your Budget and Your Employees.

SimplyHRA helps small businesses and startups replace traditional group health plans with a flexible ICHRA. You set a fixed monthly budget, your employees choose the plans that fit their lives, and we help with enrollment, compliance, and ongoing support.

Instead of dealing with annual renewal increases and one-size-fits-all coverage, you can offer a more personalized health benefit with clearer costs and less administration.

Instead of dealing with annual renewal increases and one-size-fits-all coverage, you can offer a more personalized health benefit with clearer costs and less administration.

Does any of this sound familiar?

Your group plan renews every year—and every year the price goes up.

SimplyHRA replaces that unpredictable renewal cycle with a fixed monthly contribution you set once. Your cost doesn't change unless you choose to change it.

Some employees are in states where your network barely covers anything.

With ICHRA, every employee shops for coverage in their own state and market — so someone in Colorado gets Colorado plans, not your Texas network.

You're spending hours managing renewals, benefits questions, and chasing paperwork.

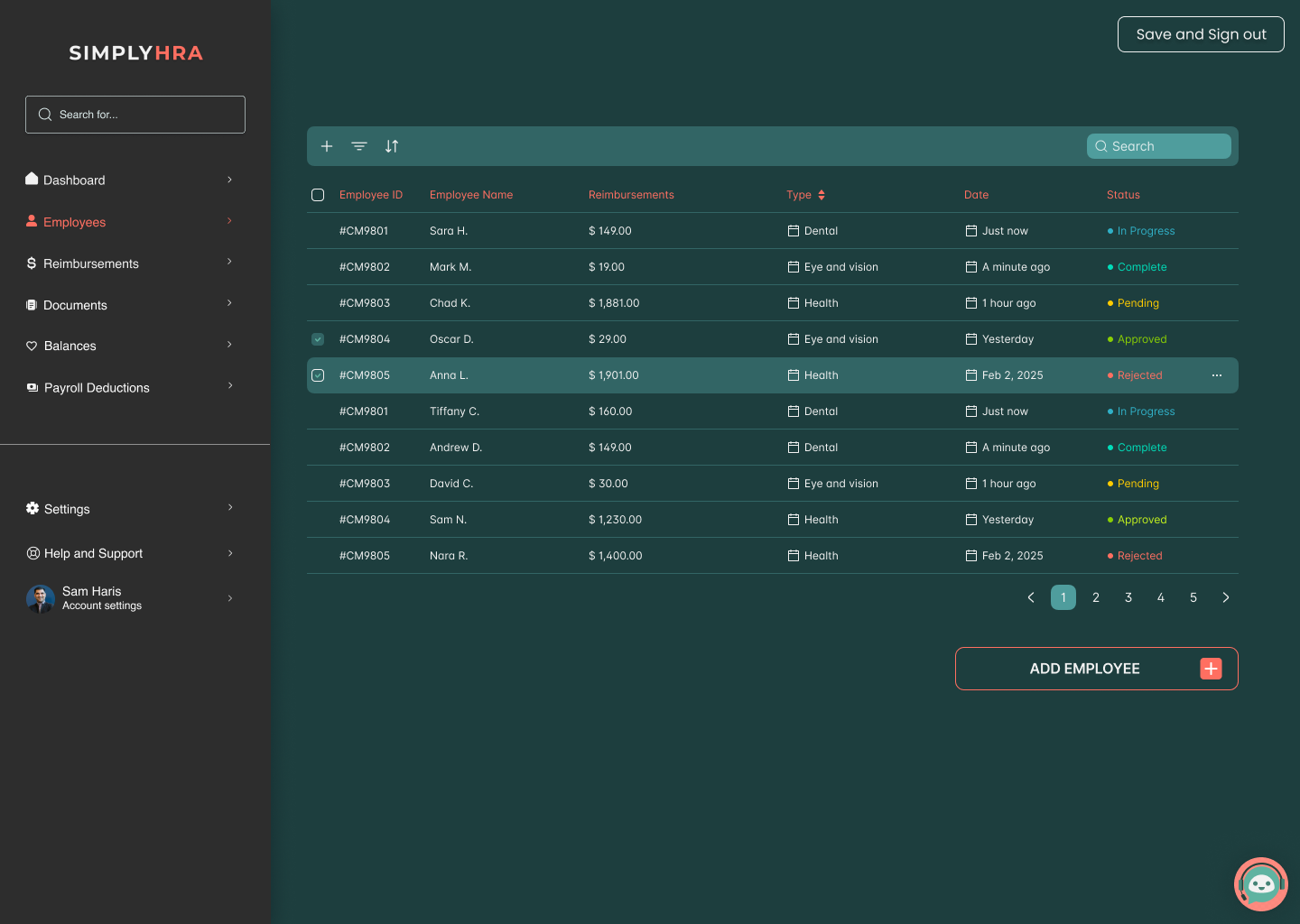

SimplyHRA handles enrollment, compliance documents, reimbursement workflows, and employee questions — so your team isn't running a benefits department.

Your team is growing in new states, but your plan wasn't built for that.

ICHRA is built for distributed teams. Add employees in any state without restructuring your plan or renegotiating a group contract. Your employees can change coverage when they move.

A smarter alternative to group health insurance

Replace unpredictable group plan renewals with a fixed monthly budget and benefits your employees will actually use.

Cost control

Set a fixed monthly budget by employee class and avoid the annual renewal surprises that come with traditional group plans. Employer contributions are generally tax-deductible, and your costs stay easier to plan.

Employee choice

Each employee can choose the plan that fits their doctors, prescriptions, family needs, and location instead of everyone being forced into the same network.

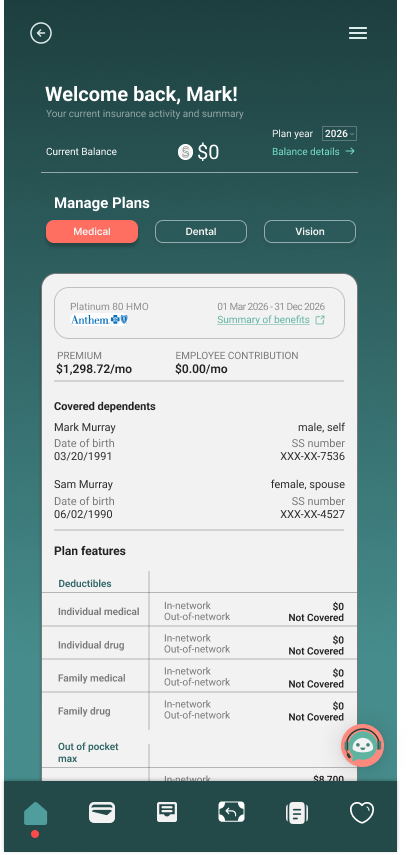

Virtual card

Employees receive a pre-funded virtual card loaded with your monthly contribution, it pays their insurance premium directly - no reimbursement forms, no 4-week waits.

Compliance

We generate plan documents, affordability calculations, reimbursement workflows, and ACA-ready reporting so your team spends less time on paperwork and more time running the business.

Benefits specialist

Every employee gets access to a licensed benefits specialist who helps them compare plans and enroll, reducing the support burden on HR. We have specialists licensed in all 50 states.

Plan flexibility

Reimburse premiums only, eligible medical expenses only, or both, and configure different amounts by employee class, location, or other qualifying categories.

Set it up one. We handle the rest.

SimplyHRA handles setup, compliance, and day-to-day administration so you can focus on running your business, not your benefits stack. Your team sets the budget — we take care of everything else.

Set Your Budget In Minutes

Choose monthly reimbursement amounts by employee class, whether by location, role, or full-time versus part-time status. Your budget stays predictable.

Employees Pick Plans That Fit Them

Each employee works with a licensed benefits specialist to compare ACA marketplace and private plan options based on doctors, prescriptions, family size, and budget.

Virtual Cards Handle Payments

Employees receive pre-funded virtual cards tied to their HRA contribution, making premium payments easier and reducing reimbursement friction from weeks to zero.

Ongoing Personalized Support

Our team and AI assistant help answer questions about eligibility, plan changes, compliance, employment changes, and support requests through email, phone, or chat.

Seamlessly integrate with your existing payroll systems

and many more!

Simple and transparent pricing

No setup fees. No onboarding fees. No platform fees. No switching fees. One price. You only pay for employees who are enrolled. If an employee doesn't participate, there's no charge.

No hidden fees.

$29/mo

per employee

Set up your ICHRA plan in minutes.

Licensed benefits specialist for every employee, included.

Audit-ready compliance reports and plan documents.

Employee reimbursement requests and approvals handled in one place.

Employer-to-employee reimbursement payments, automated.

Virtual card for direct premium payments.

Automatic expense classification and partial reimbursements.

Priority + onboarding customer support

What employers and their teams are saying

Hear from the employers and employees who've already made the switch.

"I hated having to deal with group plan drama every year. SimplyHRA empowered everyone on my team to manage their own healthcare while I set an annual budget. No more drama! Plus my accountant is happier."

Owner, Small Business

"SimplyHRA has been the easiest way to get setup with ICHRA for myself and my team. I used their benefits specialist to find new healthcare plans and couldn't be happier as an employer and W2 employee."

YC Founder

"We were paying extra with another tool that was really just using a spreadsheet. SimplyHRA makes administering ICHRA easy but the real value to me as an employee is the support I get managing my personal healthcare."

HR Manager, Small Business

"I was nervous about losing my group plan but SimplyHRA's benefits specialist found me one within a week that allows me to keep my doctor while paying less out of pocket. The virtual card pays my premium on auto-pay."

Employee receiving HRA Benefits

Employer ICHRA FAQs

Here are the questions employers usually ask when they’re comparing ICHRA to a traditional group plan or another platform.

How does the virtual card work?

Each enrolled employee receives a virtual card funded with the employer’s monthly HRA contribution. The card is used to help pay eligible insurance premiums, reducing reimbursement friction and giving employees an easier payment experience. Employees can add it to Apple Wallet or Google Pay, or enter the card number in their carrier's payment portal.

What happens if an employee doesn't enroll in health coverage?

If an employee does not enroll in qualifying individual health coverage, they do not receive HRA reimbursements. You only pay for employees who are actively participating.

Can I offer different amounts to different employees?

Yes. ICHRA rules allow employers to create eligible employee classes and set different reimbursement amounts based on those classes.

Are business owners eligible to participate?

C-Corp owners with W2's are eligible. Other business types do not currently qualify for their owners to claim HRA benefits.

How long does setup take?

Most employers are fully onboarded in 2–3 weeks. Employees typically receive virtual cards within 3–5 business days after completing enrollment requirements.

Is the HRA contribution pre-tax or post-tax?

For employers, HRA contributions are generally a pre-tax business deduction. For employees, the reimbursement is tax-free when used for eligible coverage and expenses.

What payroll systems do you work with?

SimplyHRA supports employers using major payroll and HR systems, and setup details can be reviewed during onboarding or consultation.

What happens if an employee doesn't accept the HRA offered?

You don't pay. SimplyHRA only charges for employees who are actively enrolled in the platform. If an employee declines or hasn't enrolled, they are not billed.

Still have questions?

Can’t find the answer you’re looking for? Contact us! We're here to help.

HRA blog, glossary, and more

Employer guides, ICHRA explainers, and compliance resources.

Does My Health Plan Qualify for an ICHRA? A Plan-by-Plan Guide

Marketplace, Medicare, COBRA, a spouse's plan — see exactly which health plans qualify for an ICHRA and what to do if yours doesn't.

Read post

SimplyHRA vs Take Command

Compare SimplyHRA and Take Command to find the best ICHRA platform for your business based on pricing, company size, features, and compliance automation.

Read post

Waiting Period

Clear guidance on ACA 90-day waiting periods, ICHRA timing, common mistakes, and best practices for small business compliance and employee communication.

Read post

W-2 Safe Harbor

Understand the W-2 Safe Harbor for ACA affordability: how it works, employer responsibilities, common pitfalls, ICHRA interaction, and compliance tips.

Read post

Ready to Cut Your Benefits Costs and Give Employees Better Coverage?

Book a free 15-minute call. We'll walk you through how ICHRA compares to your current plan, what setup looks like, and what you'd pay ($29 per employee per month).

Fixed monthly cost - no renewal surprises.

Employees pick plans that fit their lives.

We handle compliance, payments, and support.