ICHRA Defined Contributions: A Guide for Brokers in 2026

ICHRA Defined Contributions: A Guide for Brokers in 2026

Individual Coverage Health Reimbursement Arrangement (ICHRA) is an employer-sponsored benefit designed for flexibility and cost control — the perfect antidote to skyrocketing healthcare costs.

While ICHRA is rising in popularity, a large number of businesses are still reluctant to transition from the model they're familiar with, which is usually a traditional group health plan.

Sure, it's easy to draw parallels between ICHRA and group plans, especially in terms of tax advantages and employer-sponsorship. But they're also different enough to make most employers uncomfortable when contemplating a transition.

That's where you, the broker, should step in.

By bridging knowledge gaps around ICHRA strategy, compliance, and costs, you assume the role of an indispensable strategic advisor — helping clients confidently make informed decisions regarding employee healthcare.

An effective strategy is to start highlighting the key differences between ICHRA and traditional group health plans. And, in this post, we'll focus on the fundamental shift between each plan's contribution structure: from percentage-based to defined contributions.

Let's dive right in.

Understanding Defined Contributions

Most employers that offer group health plans offer percentage-based contributions.

This is designed to complement cost volatility while ensuring employees are adequately and fairly supported when it comes to their healthcare needs.

For example, if an employer's percentage-based contribution is 85%, employees only need to cover the remaining 15% of their group plan's premium.

While the exact contribution percentage varies by company, the usual split is around 80-20 (employer-employee) for single coverage and 70-30 for families.

For most employers, percentage-based contributions are simple, familiar, and comfortable — so much so that they might overlook the fact that defined contributions edge out percentage-based contributions in terms of cost control and predictability.

Here's how defined contributions work in a nutshell:

- Specifying Employee Classes — Start by defining which eligible employee classes will be offered ICHRA.

- Planning Your Allowance Model — Set specific monthly reimbursement allowances per employee class.

- Managing Compliance — Ensure you abide by applicable compliance rules (e.g., minimum class size and affordability).

Rather than percentage values, a defined contribution is a fixed dollar amount that employers offer to reimburse their employees' healthcare costs. This includes their monthly individual insurance premiums and other eligible, out-of-pocket medical expenses.

Let's say your client's ICHRA plan provides $700 per month as reimbursement allowance.

There's no need to worry about fluctuating premiums or renewal costs. Once your client's reimbursement budget is set, that will dictate their monthly contributions — full stop.

For example, if an employee only needs $600 a month to cover their insurance, they can use the remaining $100 for other eligible expenses (e.g., maternity care, prescription drugs, and vision exams). But if premiums rise to $720, employers are under no obligation to increase their monthly reimbursement allowances to make up the difference.

ICHRA also has another key advantage over traditional group plans in terms of flexibility.

While traditional group plans provide uniform benefits to all enrolled employees, ICHRA gives employers the ability to tailor reimbursement plans to different employee classes. This adds another layer of customizability to your defined contribution strategy.

Building Your Defined Contribution Strategy

Learning the benefits of ICHRA and defined contribution is just the first step.

Your next objective is to ensure your strategy is airtight in terms of costs, employee satisfaction, and compliance.

Let's take it step by step:

1. Defining Eligible Employee Groups

To help your client determine the sweet spot for defined contributions, start from the ICHRA-eligible employee classes approved by the IRS:

- Full-time employees — Employees that work 32-40+ hours a week.

- Part-time employees— Employees doing fewer than 32 hours a week.

- Salaried employees — Employees that earn a fixed income.

- Non-salaried employees — Employees paid on a piece-rate, shift-based, or hourly basis.

- Employees in specific rating areas — Employes based on specific ACA rating area or state.

- Employees through a staffing firm — PEO-leased employees (or sourced from a temp agency).

- Seasonal employees — Temporary hires (usually for periods of six months or less).

- Covered by bargaining agreement — Employees tied to a Collective Bargaining Agreement (CBA).

- Employees within the waiting period — New hires within the permissible, 90-day waiting period.

- Non-resident aliens with no US-sourced income — Overseas employees who don't live in the US.

- Any combination of the employee classes above.

Remember, different employees have different needs, and it's crucial for employers to have a firm grasp on what adequate healthcare looks like for each eligible employee class.

Employees who work in an expensive rating area like Vermont and Wyoming, for example, may need a higher allowance than those from affordable states like Minnesota and Maryland. The same can be said for full-time workers, who may require more robust coverage compared to part-time workers.

While thorough deliberation is required to arrive at a fair number for each employee group, understanding the IRS-approved employee classes is a huge step in the right direction.

2. Verifying Compliance

Picking employee classes narrows down your work to who are actually eligible for ICHRA.

The next step, which focuses on compliance, lays down non-negotiable baselines that will simplify the rest of the process.

Let's start with the affordability rule, which involves Applicable Large Employers (ALE).

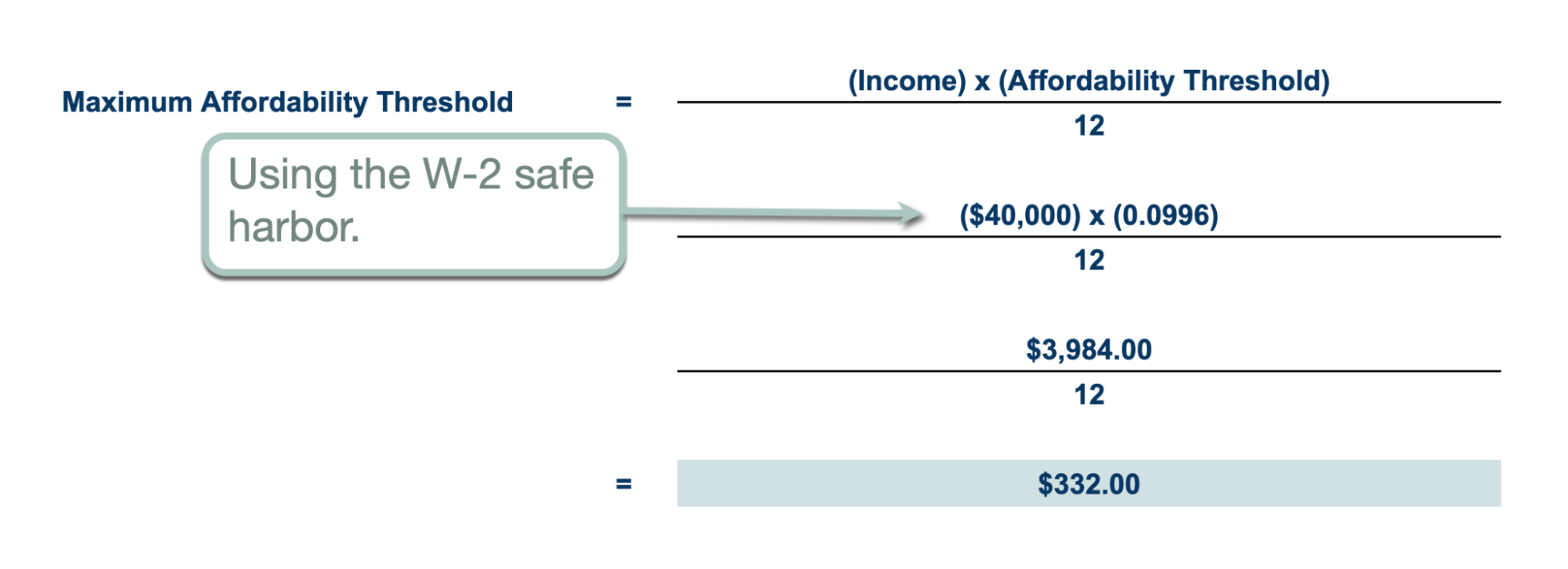

Basically, if your client qualifies as an ALE (having 50 or more FTE employees), they need to make sure their ICHRA is "affordable." This means the employee's share of monthly health insurance premiums through ICHRA must not exceed 9.96% (affordability threshold for 2026) of their annual household income.

While using the Lowest Cost Silver Plan (LCSP) as a benchmark, this threshold is compared against three possible safe harbors as defined by the IRS:

- W-2 wages

- Federal Poverty Line (FPL)

- Rate of Pay (hourly rate x 130 hours — or monthly salary)

Suppose John is an employee at your client's company who makes $40,000 in W-2 wages. And, in his rating area, the monthly premium for the LCSP is $750.

We can determine the maximum affordability threshold using the following formula:

With $332 as the employee's affordability threshold, the employer must provide at least $418 to make their ICHRA affordable (for purchasing the LCSP at $750).

As long as employees aren't required to pay more than the affordability threshold, the ICHRA is affordable and therefore compliant (if your client classifies as an ALE).

This establishes a baseline for your client's defined contribution strategy.

As far as compliance goes, ALEs also need to make sure their ICHRA is offered to at least 95% of FTE employees. And should they decide to offer ICHRA and traditional group plans side by side, below are a few compliance checkboxes to remember:

- An employee cannot choose to participate in ICHRA and the employer's group plan at the same time.

- If your client has fewer than 100 employees, their ICHRA should have at least 10 participants.

- If your client has 100-200 employees, their ICHRA must cover at least 10% of their entire workforce.

- If your client has over 200 employees, their ICHRA must have at least 20 participants.

Important: Conduct in-depth research on the affordability thresholds that apply to your client's eligible employee classes. Be thorough with your data-gathering process, like the LCSP for all relevant rating areas.

3. Finalizing Your Allowance Model

Once you have your employee classes and minimum, affordability-compliant amount, it's now just a question of "how high should you go?"

For starters, brokers should encourage clients to focus on the pricing of Gold and Silver plans in relevant rating areas.

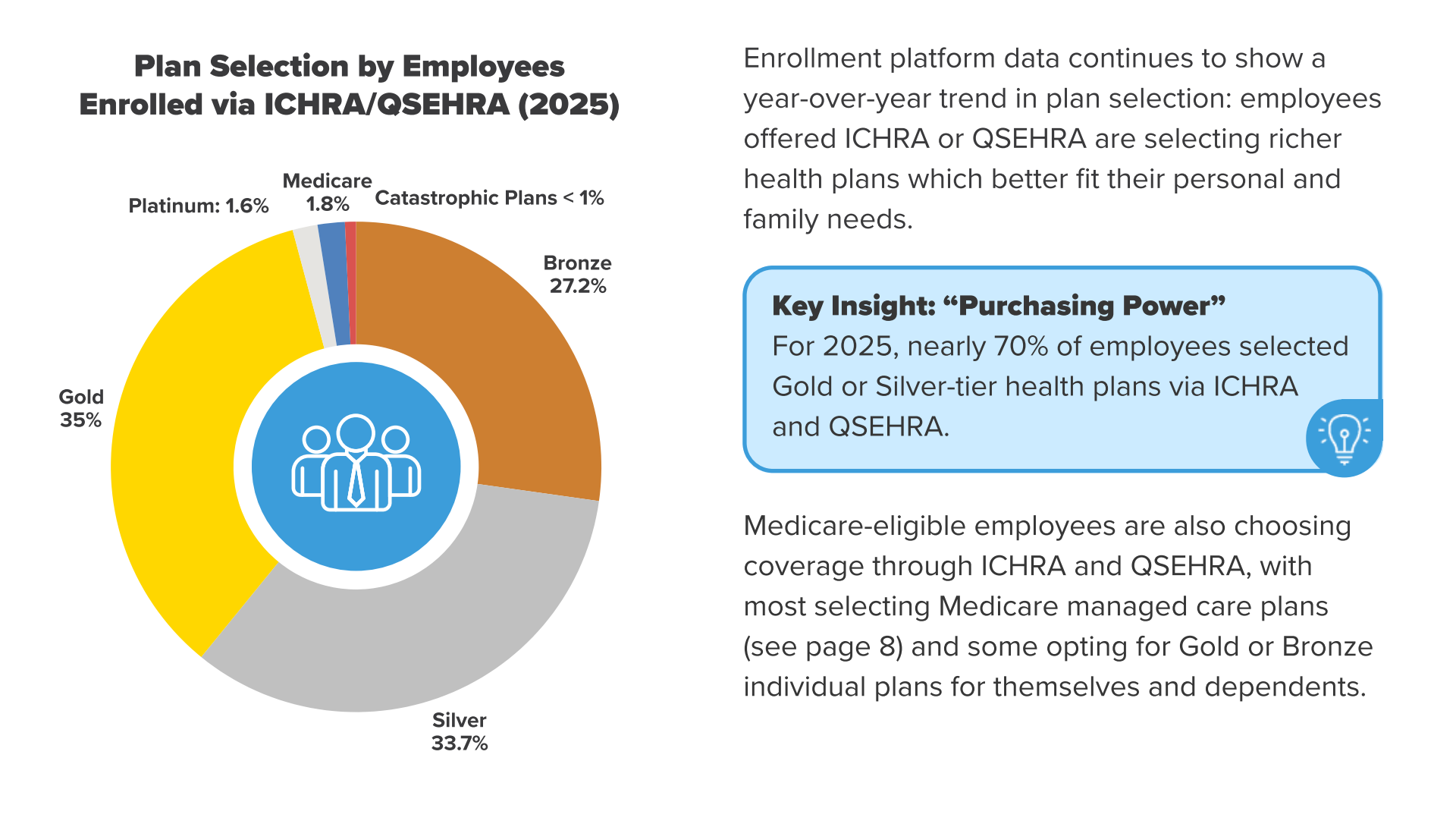

According to the HRA Council's 2025 Growth Trends Report, roughly 70% of employees under ICHRA choose Gold and SIlver-tier plans. As such, companies need to use their prices as basis when planning their allowance models.

It's also useful to review other HRA Council reports and broker surveys to give clients an idea of how much their competitors are offering through ICHRA. This is especially important if they value the impact of ICHRA when it comes to attracting and retaining talent.

Lastly, a lot of employers also miss out on the opportunity to optimize their ICHRA contribution strategy based on age and number of dependents.

After all, employees with dependents will naturally have higher healthcare costs than those looking for individual coverage.

There are two ways to go about this:

- Manually configure different ICHRA plans per class that account for the employee's age, number of dependents, or both.

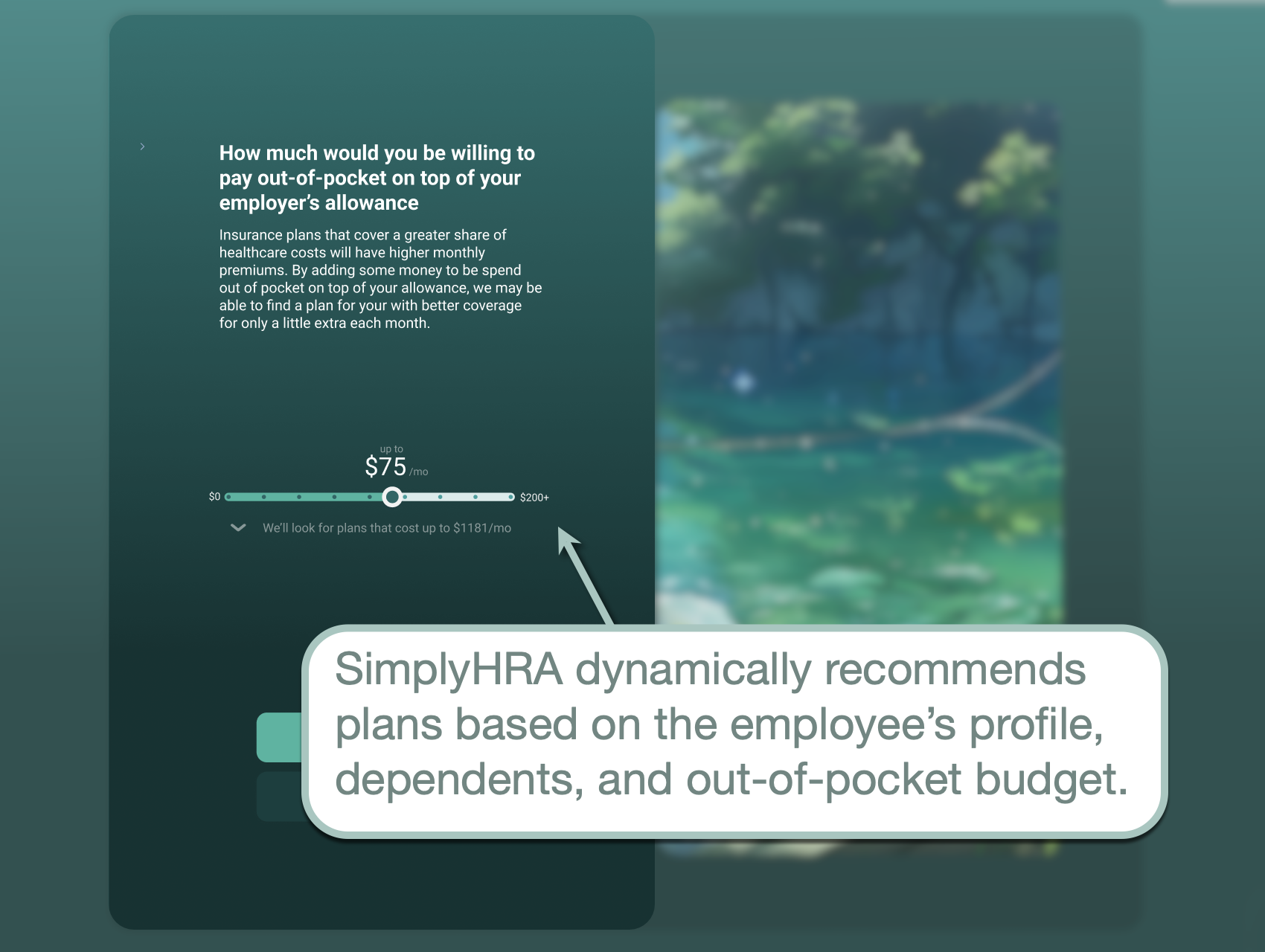

- Use a benefits platform like SimplyHRA that algorithmically recommends insurance plans based on employee class and the employee's maximum out-of-pocket budget.

Should your client prefer the manual approach and create various plans based on age, remember to observe the 3:1 ratio rule. This means the oldest age bracket can only receive up to exactly three times more than the youngest.

For example, if ICHRA offers $600 to the oldest bracket within a specific employee class, the youngest bracket must receive at least $200 — maintaining the 3:1 ratio ($600:$200).

With a benefits platform like SimplyHRA, employees can get personalized plan recommendations by entering details of their dependents and maximum out-of-pocket budget.

These recommendations are made available in real time. Employees only need to set their profile properly through the desktop or mobile dashboard.

Conclusion

Defined contributions may seem intimidating at the surface, especially for companies coming from the familiar percentage-based contribution. But once you and your clients understand how it works and its benefits, it becomes clear that ICHRA is the superior choice if you value flexibility, predictability, and streamlined compliance.

Hopefully, the guide above answered all of your questions regarding ICHRA and defined contributions.

If you have further questions or are in the market for an ICHRA-focused benefits platform, don't hesitate to reach out to us here.

Cheers!

Related blogs

Should I Buy a Pre-Funded ICHRA Debit Card? 2026 Guide

How Employees Reconcile APTC After Joining Employer HRA 2026