Can You Use ICHRA With ACA Tax Credits (2026)?

Some say Individual Coverage Health Reimbursement Arrangement (ICHRA) is the future of healthcare — and there are plenty of reasons to believe it.

It offers predictable costs, customizable benefits per employee class, tax-advantaged transactions, and easy administration. That covers practically every pain point that businesses have with traditional health plans.

However, not everybody is familiar with how ICHRA works. And for those people, one of the burning questions is whether or not ICHRA and ACA tax credits are compatible.

Let's face it, tax credits are a massive help for individuals and families amidst the rising healthcare costs. And broadly speaking, employees covered by ICHRA are not eligible to claim premium tax credits (PTC).

But that doesn't mean employees who are offered ICHRA are ineligible for tax credits outright.

Read on to learn more about PTC, how tax credits interact with ICHRA, and other crucial details to help employees make an informed decision.

What are Premium Tax Credits?

In simple terms, PTC pertains to government-funded subsidies designed to help individuals and families pay for health insurance premiums.

PTC values are based on the applicant's projected income for the current year. The basic idea is simple: the lower your income, the bigger your tax credit.

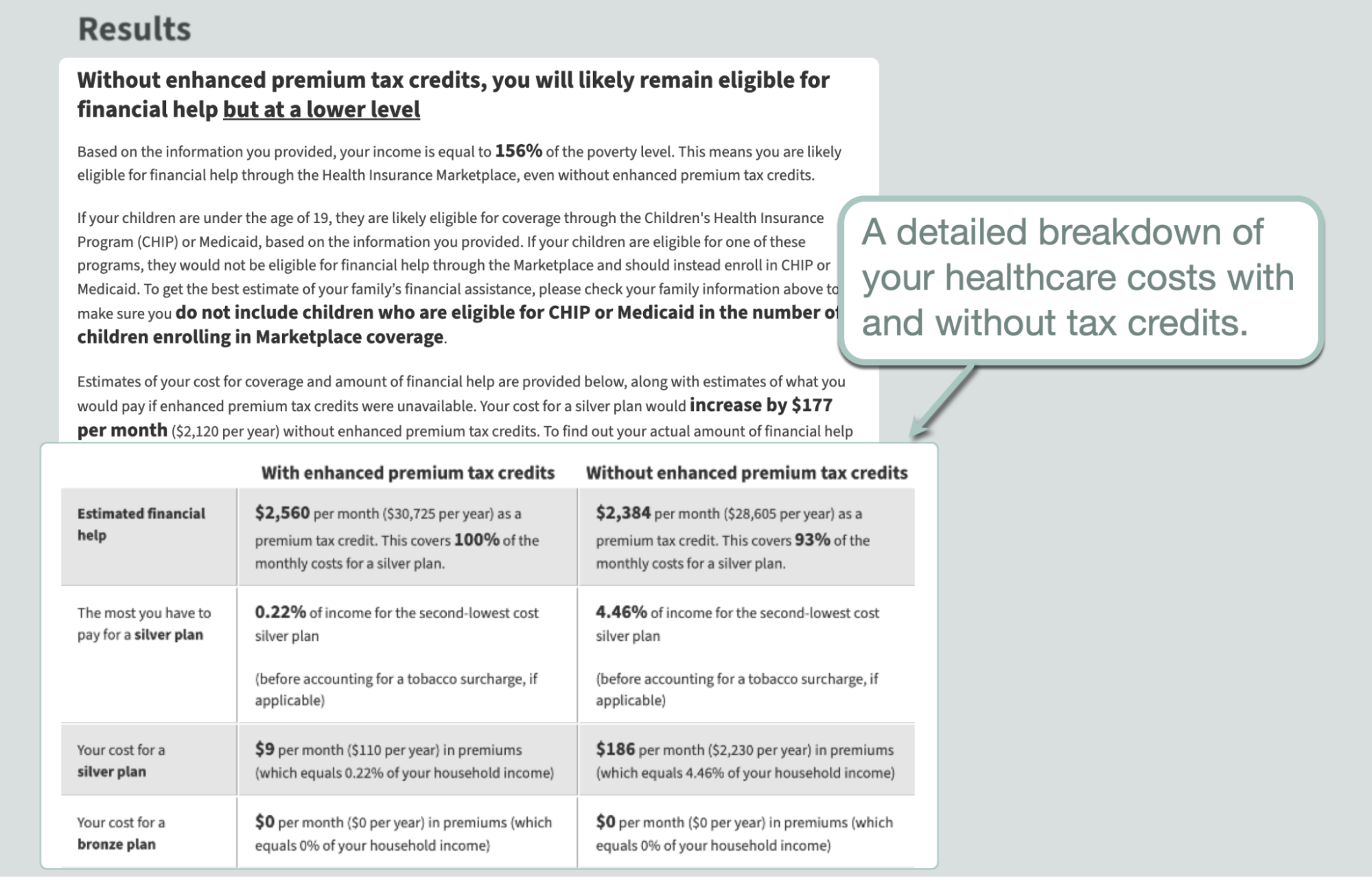

You can use tools like the KFF ACA Enhanced Premium Tax Credit calculator to get an estimate. Just enter important details about your household, including your state, yearly income, and number of dependents.

Within seconds, the calculator will generate a detailed breakdown of your healthcare costs, including how much you'll pay in premiums with tax credits for a silver and bronze plan.

It's worth noting, however, that underestimating your projected income when claiming PTC means you need to reconcile the excess come tax time.

Suppose your projected household income is $35,000 for the year.

After applying for PTC, you received $720 per month to pay for your Silver plan.

However, it turns out you actually made $45,000 that year — meaning you were only actually eligible for $600 per month in PTC.

That's an overpayment of $120 per month, which means you owe the IRS $1,440 ($120 multiplied by 12) when you file your federal income tax return.

Of course, there are some cases where the opposite is true. If you underestimated your income and received less in PTC than you're actually eligible for, the IRS will send you a refund instead.

Who Qualifies for PTC?

The IRS published clear guidelines when it comes to PTC eligibility under the ACA.

In summary, you can collect tax credits under the following conditions:

- You must have a household income within the eligible range.

- You must purchase insurance through the Marketplace.

- You must file a federal income tax return.

- You must not be eligible for public coverage (e.g., Medicaid, CHIP, and military coverage).

In addition to these conditions, employees are also not qualified to get tax credits if their employer offers health coverage that's considered "affordable" and provides minimum value (covers at least 60% of health costs).

This ties us back to ICHRA…

Understanding ICHRA: Why It Conflicts with PTC

Although ICHRA is a highly flexible benefit that enables a deep level of control, some compliance boxes need to be checked, especially if you're an Applicable Large Employer (ALE). This means your company has 50 or more Full-Time Equivalent (FTE) employees.

For one, plans purchased through ICHRA must satisfy the minimum value requirement under ACA rules. This means the plan should cover 60% of the costs of standard medical services as well as offer substantial coverage for physician and inpatient hospital services.

Furthermore, large employers must also observe the ICHRA affordability rules set by the Tri-Departments, namely:

- U.S. Department of Health and Human Services

- U.S. Department of the Treasury

- U.S. Department of Labor

Under the affordability rule, the employee's premium contribution throughout the plan year shouldn't exceed 9.96% of their annual household income (2026). This affordability threshold changes every year, so be sure to check official sources for future plan years.

For reference, here's a roundup of the affordability thresholds from 2020:

Year

Affordability Threshold

2020

9.78%

2021

9.83%

2022

9.61%

2023

9.12%

2024

8.39%

2025

9.02%

2026

9.96%

Applicable Large Employers must evaluate ICHRA affordability for employer shared responsibility purposes. ALE status alone does not make every ICHRA offer affordable or automatically block tax credits. An employee offered an unaffordable ICHRA may qualify for a Marketplace Premium Tax Credit only after opting out, assuming the employee meets the other eligibility requirements.

As for employees, they only need to be enrolled in a qualifying Minimum Essential Coverage (MEC) plan in order to participate in ICHRA. The good news is, they're now a part of a tax-advantaged plan that can support an employer-specified list of medical expenses.

For other questions regarding affordability and ICHRA in general, don't hesitate to contact us here.

Is My ICHRA Plan Affordable?

To calculate if your company's ICHRA plan is affordable, you need to look at the Lowest-Cost Silver Plan (LCSP) in your employees' ACA rating area.

This will be your benchmark when determining your ICHRA plan's affordability.

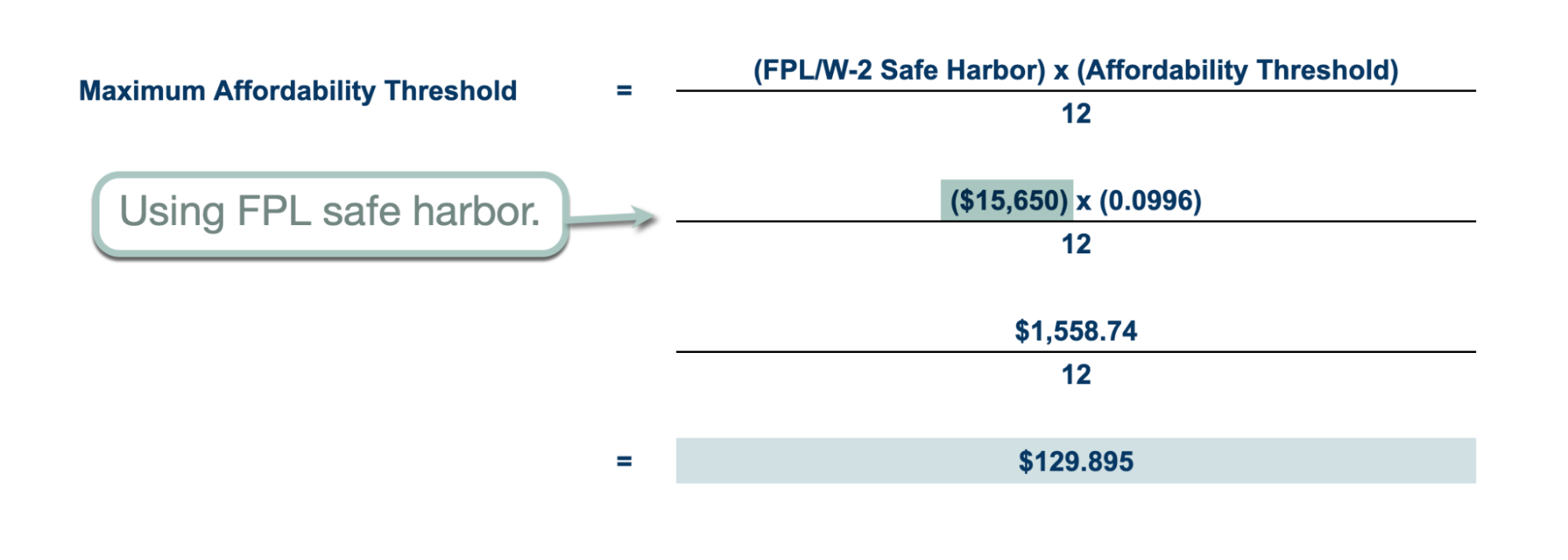

From that figure, subtract your ICHRA monthly allowance to get the employee's required contribution:

You then have to make sure this amount doesn't exceed the maximum affordability threshold per month. This is calculated by multiplying your employee's annual household income by the affordability threshold percentage (9.96% for 2026) and dividing the result by 12.

Take a look at the formula below:

For example, if the LCSP in your employee's ACA rating area costs $720 and your monthly ICHRA allowance is $600, their share of the premium would be $120.

Since this is lower than the maximum affordability threshold ($129.90), your ICHRA plan is considered "affordable." In such a plan, it's worth noting that your employees will not be eligible to claim ACA tax credits.

When Employees Can Choose PTC Over ICHRA

Here's the thing: Small businesses (fewer than 50 FTE employees) are not legally required to follow the affordability rule when offering ICHRA. Unlike ALEs, they don't have to worry about ACA penalties if employee contributions to their ICHRA exceed the affordability threshold.

If the plan is not "affordable," employees may consider opting out of ICHRA and using the Marketplace instead, making them eligible to collect tax credits.

This makes perfect sense if the employee's monthly ICHRA contributions will be higher than their PTC-covered monthly premiums.

For example, let's say an employee's annual household income is $38,000, putting their maximum affordability threshold at $315.40 per month (using W-2 safe harbor).

If your ICHRA offer is $400 per month and the LCSP monthly premium is $750, we can calculate that their required contribution is $350 (LCSP premium minus ICHRA allowance) — higher than their maximum affordability threshold ($315.40).

This deems the ICHRA unaffordable, which makes the employee eligible for PTC.

With a PTC amounting to $434.60, the employee also ends up paying less per month than if they participate in their employer's ICHRA.

After all:

- With ICHRA: The employee contributes $350 per month ($750 minus $400)

- With PTC: The employee only contributes $315.40 per month ($750 minus $434.60)

Just remember that, should employees decide to opt out, they need to make a final decision before the ICHRA plan's start date.

Final Words

To wrap things up, remember the following takeaways:

- Employees can't use ACA tax credits if their employer offers an "affordable" ICHRA plan.

- If the ICHRA plan is "unaffordable," employees can opt out and use tax credits for a Marketplace plan.

- Employees can't participate in ICHRA and use PTC at the same time.

Ensuring your ICHRA plan is affordable is crucial for ensuring successful implementation. Learn more about ICHRA and how it can benefit your organization by reaching out to us here.

Related blogs

Does My Health Plan Qualify for an ICHRA? A Plan-by-Plan Guide

SimplyHRA vs Take Command