Top 5 Benefits of Implementing ICHRA in Your Startup

Employers with at least 50 full-time-equivalent employees may be applicable large employers subject to the ACA employer mandate. They generally must offer qualifying coverage to full-time employees and dependents or may face penalties; an affordable ICHRA can be one compliant option.

However, employee healthcare is more than just a checkbox on your compliance list. It also provides numerous benefits that optimize productivity and sustainable, long-term scalability.

In this post, we'll take a look at Individual Coverage Health Reimbursement Arrangement (ICHRA) — a type of account-based healthcare plan — and why you should consider it.

But first, a quick introduction.

What is ICHRA?

ICHRA is a healthcare plan that works by providing employees with reimbursement allowances for qualified medical expenses, including health insurance premiums. While it requires employees to have individual health insurance coverage to participate, it also unlocks a ton of benefits in terms of flexibility, risk management, employee satisfaction, and administration.

Top 5 Benefits of ICHRA for Startups

Here's a closer look at the benefits of ICHRA for startups and small businesses:

1. Cost Control & Predictability

One of the key advantages of ICHRA is complete cost control for employers.

As an employer, you're in charge of setting the monthly reimbursement allowances per employee class. There are no minimum and maximum contribution limits, either — unlike other HRA types like Qualified Small Employer Health Reimbursement Arrangement (QSEHRA) with capped contribution limits set by the IRS.

With control over reimbursement allowances, your employee healthcare budget is stable and predictable. This effectively takes care of the risk aspect of employee health benefits.

2. Tax Efficiency

When it comes to employee healthcare, ICHRA has three main advantages when it comes to taxes.

For one, monthly contributions by employers are tax-deductible as a business expense. This also benefits employees by reducing their taxable income.

Additionally, approved ICHRA reimbursements for eligible medical expenses and insurance premiums are 100% tax-free, allowing employees to reap the full benefits of their coverage.

3. Scalability

Without maximum contribution limits and total cost control, ICHRA plans can be tailored to suit businesses of all sizes.

ICHRA also has no restrictions pertaining to employer size. You could have as few as one employee or thousands of hands on deck — you're free to adopt ICHRA to provide your workers with the healthcare they deserve.

Employers can also create different ICHRA plans for specific employee groups.

For example, employees in the field who frequently travel or perform physically laborious work may be entitled to higher monthly allowances than those who stay in the office.

4. More Freedom for Employees

ICHRA also benefits employees in the form of flexible coverage options.

While employers assign the budget, employees can choose the healthcare services they need in addition to the individual health insurance product they prefer. Employees enrolled in eligible High Deductible Health Plans (HDHPs) can also integrate their ICHRA with an HSA (though the HRA cannot directly fund the savings account), which has become a more appealing strategy after the OBBBA changes in 2026.

Eligible medical expenses generally follow IRC §213(d), subject to the plan document and substantiation rules.

5. Streamlined Administration

Finally, ICHRA can be implemented either through external administrators or self-service solutions.

The process is as simple as understanding employee needs and setting adequate monthly reimbursement allowances. And with visual platforms like SimplyHRA, you'll have all the tools you need for everything — from setting monthly allowances to approving reimbursements — in one user-friendly interface.

How to Implement ICHRA with SimplyHRA

SimplyHRA is a visual, What You See Is What You Get (WYSIWYG) app for creating and managing ICHRA plans.

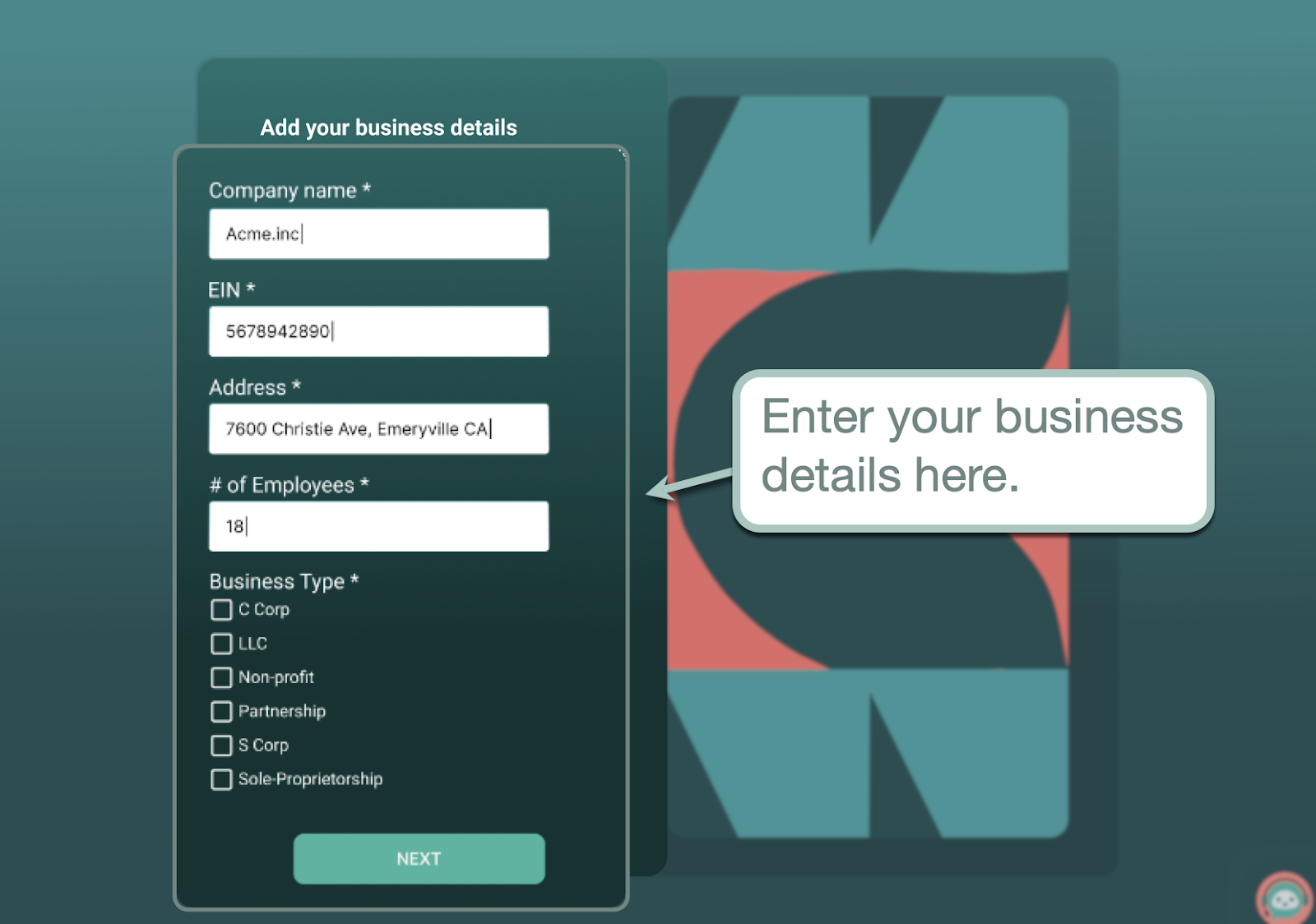

The initial setup process only involves entering essential details about your business, like your registered company name, EIN, address, and business type.

After setting up your business profile, you get to create your first ICHRA plan right away.

This can be done in only three steps:

- Step 1: Enter a name for your ICHRA plan.

- Step 2: Define the employee class you want to cover.

- Step 3: Set the monthly reimbursement allowance.

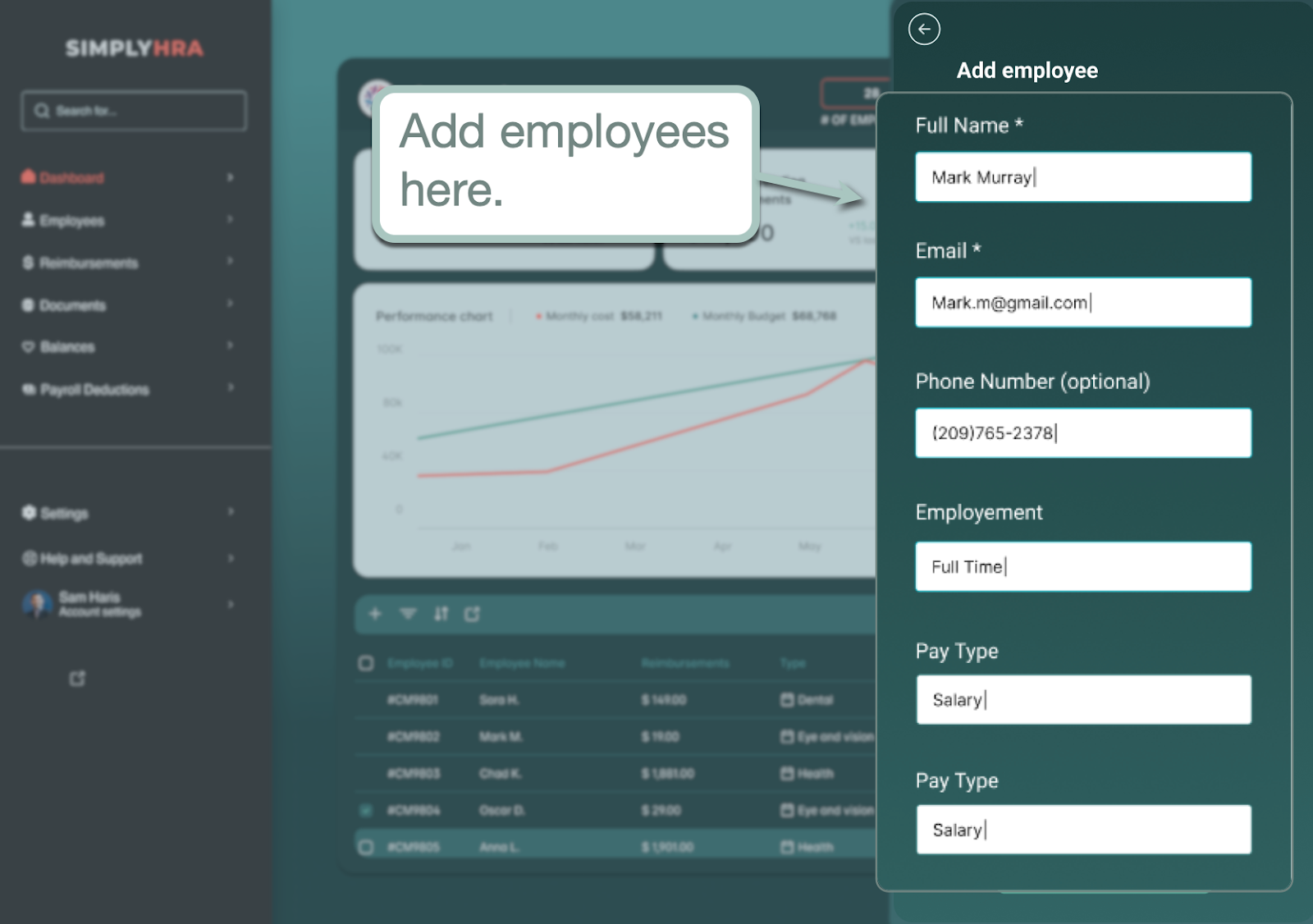

That's it — you're ready to add employees to your ICHRA plan.

Simply enter their name, contact information, employment status, and salary type.

Once enrolled, employees can also use SimplyHRA to upload reimbursement requests (along with verification documents) and track their status.

Requests can then be reviewed, approved, and denied by your designated administrator, who can also be onboarded through the SimplyHRA dashboard.

Apart from the usability factor, below are the top benefits of using SimplyHRA for managing your ICHRA plan:

- Built-in AI assistant — The SimplyHRA chatbot can answer questions, provide status updates, and more.

- Analytics reporting — Track your ICHRA budgets and spending over time.

- Cross-platform app — Use SimplyHRA on any desktop or mobile device.

- Done-for-you compliance — Focus on managing your ICHRA plan while we handle all the paperwork and compliance-related headaches on your behalf.

Conclusion

The demand for ICHRA is on the rise, and it's easy to see why.

Compared to other employee healthcare options, ICHRA offers unparalleled flexibility, scalability, cost control, and ease of administration. And as an HRA, it also grants employees the power of choice when it comes to their individual health insurance and medical expenses.

If you want to see ICHRA in action, schedule a free SimplyHRA demo today.

Professional Note: ICHRA is a group health plan subject to ERISA and Public Health Service Act requirements. Employers should maintain plan documents, provide required notices, apply eligibility rules consistently, and work with qualified advisers on fiduciary and compliance obligations.

Related blogs

Does My Health Plan Qualify for an ICHRA? A Plan-by-Plan Guide

SimplyHRA vs Take Command