2026 ICHRA Affordability Guide: How Businesses Can Stay Compliant with ACA Rules

Individual Coverage Health Reimbursement Arrangement (ICHRA) is a type of HRA or Custom Health Option and Individual Care Expense (CHOICE) Arrangement designed for flexibility and employee choice.

ICHRA eligibility must be based on permitted employee classes under federal rules; employers cannot arbitrarily include or exclude individual employees within a class. Unlike QSEHRA, which is limited to eligible small employers that are not applicable large employers, ICHRA has no upper employer-size limit.

However, ICHRA's flexibility isn't boundless.

For one, Applicable Large Employers (ALEs) with 50 or more employees are required to comply with the affordability rule under the Affordable Care Act (ACA).

Read on to learn more about ACA affordability, why it matters, and how to keep your ICHRA plan compliant.

What is the ACA Affordability Rule?

Under the affordability rule, employee contributions to their individual insurance shouldn't exceed a specific threshold of their household income.

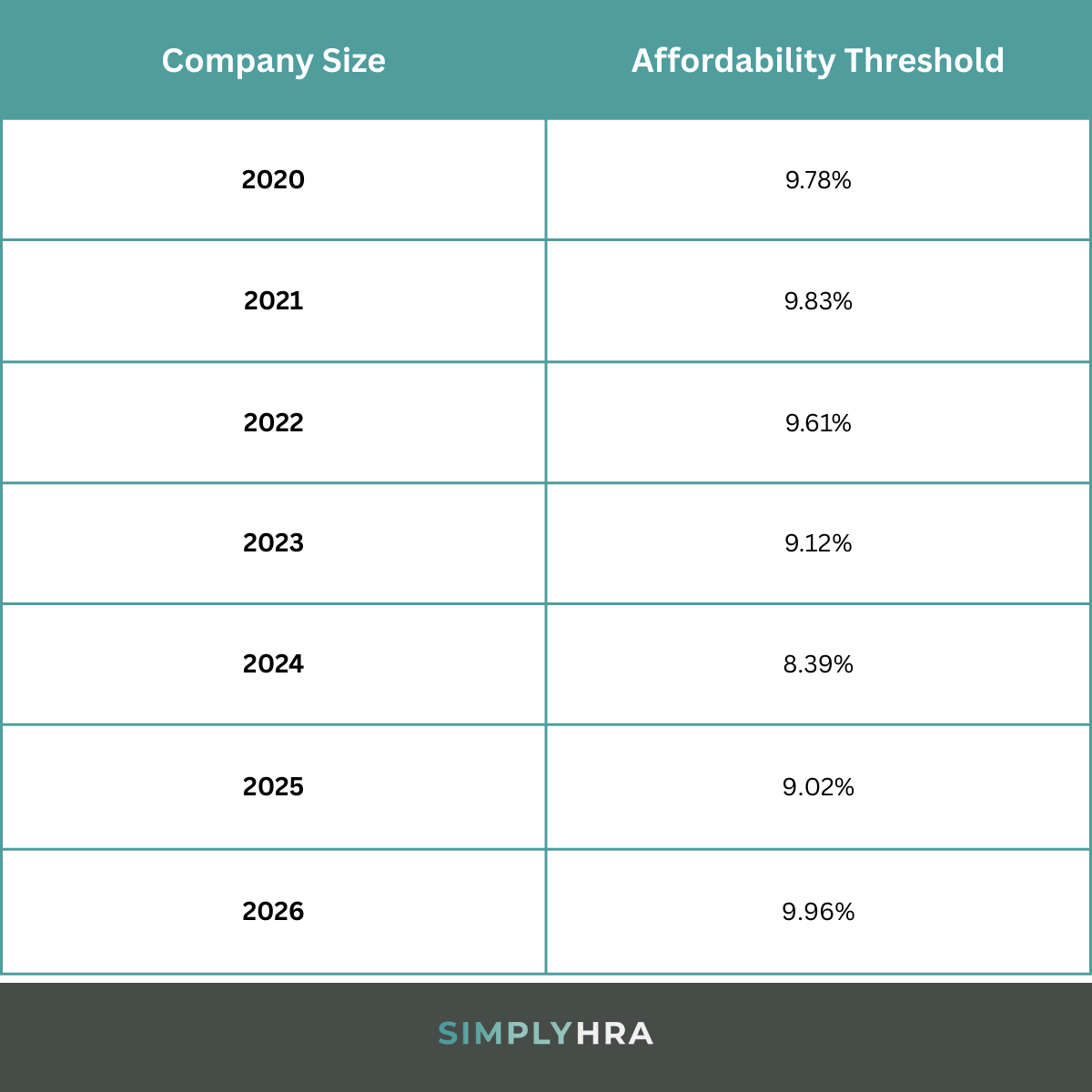

This figure changes from year to year. And, for 2026, the affordability threshold is officially at 9.96%.

This leads to the question: How can you determine if your employee's contributions fall under the threshold?

Do you need to know each of your employees' household income to calculate affordability?

Determining ICHRA Affordability

First, let's talk about the two variables you need for calculating affordability: the Lowest-Cost Silver Plan (LCSP) and the safe harbors.

When it comes to affordability, employers don't need to calculate the threshold using each employee's annual household income. Instead, you can use safe harbors that simplify your calculation:

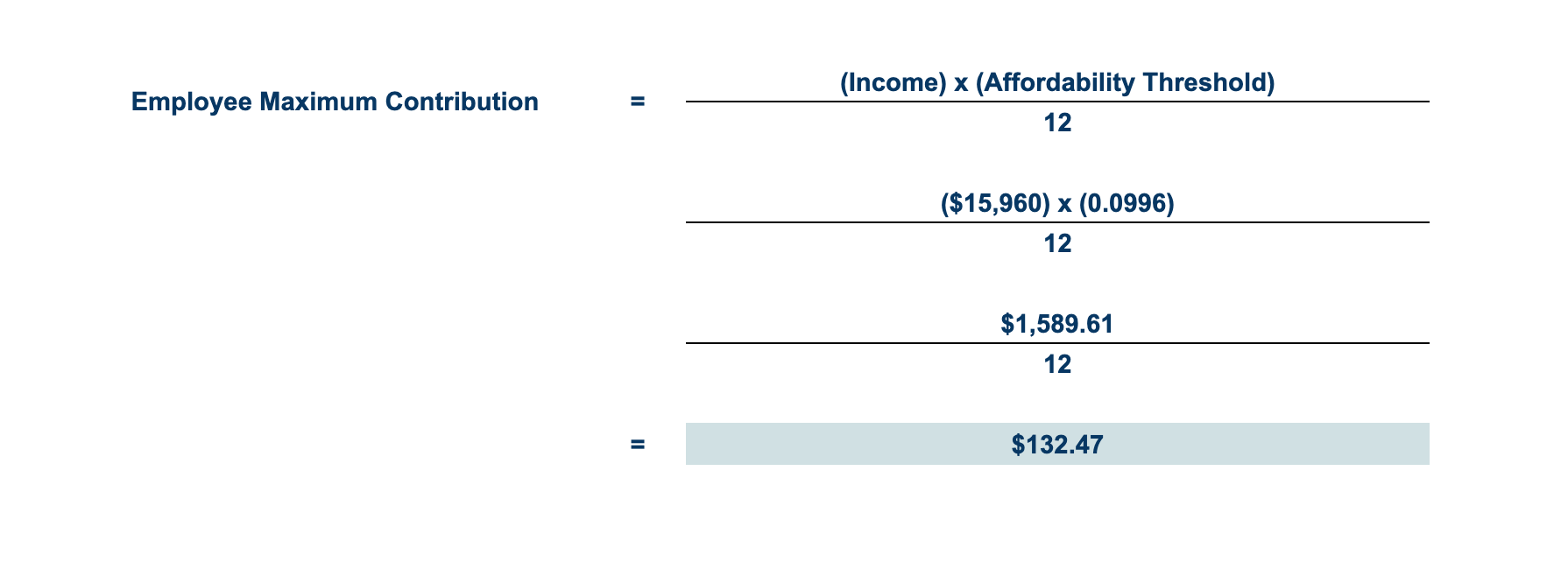

- Federal Poverty Line (FPL) — A set figure assigned to households based on the number of family members in each state. As of 2026, the FPL across the 48 contiguous states is $15,960 for a single-person household (up to $44,360 for a family of six).

- W-2 Safe Harbor — Value based on the employee's Form W-2 Box 1 Wages. Since this is retrospective (calculated at the end of the year), it can be risky for budgeting, but useful if you prefer a tad more precision when determining affordability.

- Rate of Pay Safe Harbor — Uses the annual pay of hourly and monthly salaried employees (for hourly employees, the rate is multiplied by 130 hours per month). This safe harbor can offer better flexibility than the FPL safe harbor, especially if your workforce includes higher-paid employees.

Going back to the affordability threshold for 2026, let's say you decided to use the FPL safe harbor.

That means that a single employee who makes $15,960 per year can contribute no more than $1,589.6 annually or $132.47 per month to their insurance premium.

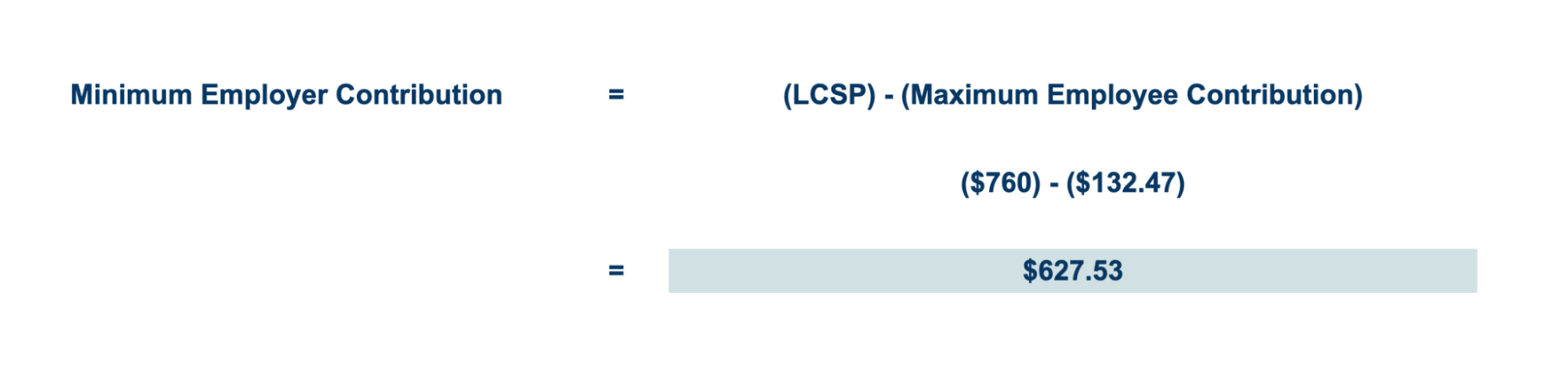

The LCSP in the employee's rating area, on the other hand, is used as the "benchmark plan" when calculating ICHRA affordability. This, of course, is something you need to check with your employees' specific rating areas.

Let's say the LCSP in your employee's area is $760 per month.

With an affordability threshold of $132.47, that means your ICHRA plan should offer a reimbursement allowance of $627.53 — at the very least — to make your plan affordable.

That's it.

You now know how to determine affordability, which is critical for ALEs looking to reap the flexibility, predictability, and customizability benefits of ICHRA while remaining compliant.

And if your ICHRA is affordable, employees who are offered participation will no longer be eligible for Premium Tax Credits (PTCs). Take note, employees are only able to decline ICHRA participation and opt for ACA subsidies if their ICHRA is unaffordable.

What are the Penalties for Violating the ICHRA Affordability Rule?

Under the ACA, employers that fail the affordability test will be subject to Employer Shared Responsibility Payments (ESRP), facing two main penalties under IRC §4980H:

- Section 4980H(a) — In 2026, employers that fail to provide Minimum Essential Coverage (MEC) to 95% of their FTE employees and their dependents will be charged an annual penalty of $3,340 per employee.

- Section 4980H(b) — Again for ALEs, failure to offer affordable coverage or minimum value coverage leads to a penalty of $417.50 monthly or $5,010 annually per employee.

ICHRA Affordability: Frequently Asked Questions

What happens if my ICHRA plan is unaffordable?

For small employers, offering an unaffordable ICHRA plan gives your employees the option to opt out and go for ACA subsidized healthcare. Employers with 50 or more employees, on the other hand, will be subject to IRS penalties amounting to $5,010 per year per employee.

Do I need to know my employees' actual household income?

No, you don't need to know or use your employees' actual household income when verifying ICHRA affordability. Instead, you can use one of the three safe harbors (Federal Poverty Line, rate of pay, and W-2 wages) to ensure employee contributions don't exceed the affordability threshold.

Does employee location affect the affordability rule?

Although the affordability threshold (9.96% for 2026) is the standard, remember that the affordability rule considers the LCSP in your employee's location. This directly affects the maximum amount employees can contribute to their insurance premiums to deem affordability.

Is the affordability threshold the same for families?

Yes, the affordability threshold of 9.96% is consistent regardless of whether the employee is single or has dependents (e.g., spouse and children). Just take note that safe harbors exist to protect businesses from penalties even without finding out each employee's actual household income.

Final Words

Affordability rule aside, ICHRA is still one of the most flexible modern health benefits in the US.

You don't have to worry about minimum or maximum contribution limits, employer size requirements, or participation minimums. In addition, employees are given the autonomy to pick their own individual health insurance product and use their ICHRA reimbursement funds on various qualified medical expenses — from doctor visits to dental procedures.

Got other questions?

Explore our library of ICHRA learning resources here. Or, schedule a free consultation and learn how to simplify ICHRA compliance through our modern benefits platform.

Related blogs

Does My Health Plan Qualify for an ICHRA? A Plan-by-Plan Guide

SimplyHRA vs Take Command